Nobody likes to contemplate death. But leaving your family to face an emotional loss alongside a bill that can run into five figures makes an already hard week even harder. Funeral expense insurance exists to close that gap: it is a small, affordable life insurance policy designed to pay for a funeral, burial, or cremation, and the loose-end expenses that show up right after a death, before an estate has been settled.

This guide breaks down exactly how funeral expense insurance works, what funerals actually cost in 2026, how policies are priced and underwritten, the tradeoffs of guaranteed acceptance coverage, and how to shop for a policy without overpaying.

How Does Funeral Expense Insurance Operate and What Is It?

Funeral expense insurance, also called burial insurance, final expense insurance, or final expense funeral insurance, is a small whole life insurance policy built specifically to cover end-of-life costs. It is not a scaled-down version of a term policy; it is a permanent contract with a modest death benefit, underwritten specifically for people who want a simple way to make sure their funeral doesn’t become a bill their family has to split.

A funeral expense life insurance policy typically works like this:

- Fixed premiums: your monthly payment is locked in at the rate you qualify for and never increases, regardless of age or health changes later.

- Cash death benefit: when you pass away, the insurer pays a lump sum directly to your named beneficiary, not to a funeral home.

- Permanent coverage: as long as premiums are paid, the policy never expires and never needs to be renewed.

It’s worth distinguishing insurance for funeral expenses from a pre-paid funeral plan. A pre-paid plan is a contract with one specific funeral home for one specific set of services. If you move or if that home closes, your money can be difficult to recover in full. A final expense insurance policy for funeral expenses instead pays cash to your family, who can use it at any funeral home.

The Rising Cost of Final Expenses: Why You Need Coverage

The case for funeral expense insurance is really a case built on real numbers. According to the National Funeral Directors Association (NFDA), the median cost of a traditional funeral with viewing and burial is $8,300, and that figure climbs to $9,995 once a burial vault required by most cemeteries is added. A full-service cremation with viewing carries a median cost of $6,280. Choosing a no-frills direct cremation, with no viewing or ceremony, brings the cost down substantially, often to somewhere between $2,200 and $5,100, depending on the provider and region.

What Actually Drives the Bill

| Expense Category | Typical Cost Range |

| Basic services & facility fee | $2,300 – $2,600 |

| Embalming & body preparation | $700 – $800 |

| Casket (metal, basic) | $2,500 – $5,000+ |

| Burial vault or grave liner | $1,400 – $1,700 |

| Transportation & hearse | $400 – $600 |

| Direct cremation (no service) | $1,100 – $2,500 |

Beyond the funeral home invoice, families are frequently blindsided by costs nobody budgets for: outstanding medical bills from a final illness, legal and probate fees tied to settling the estate, obituary and death-certificate charges, and travel expenses for relatives flying in on short notice. Individually, these often add another $2,000 to $5,000 to the true cost of a death in the family.

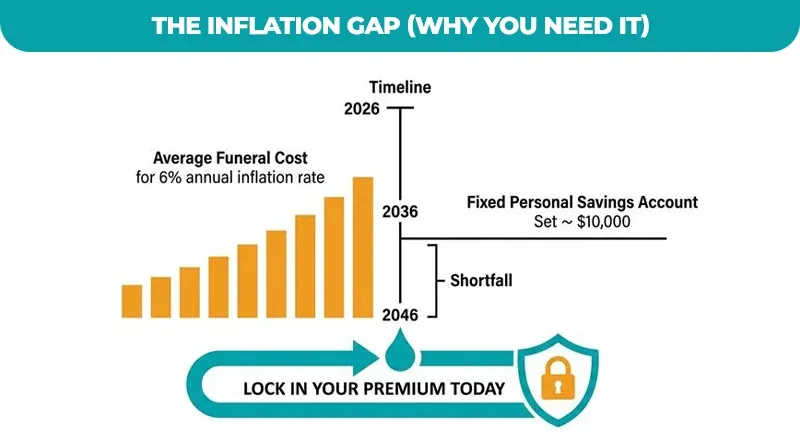

Two trends make this worse over time. First, the NFDA has tracked funeral costs rising by roughly 6% a year in recent years, faster than general inflation, which pushes the 2026 cost of a basic funeral service toward the $10,500-$11,000 range in many markets. Second, cremation has become the majority choice: the NFDA projects the 2025 U.S. cremation rate at 63.4%, up from about 30% in 2010, with adoption expected to reach 82.3% by 2045.

Types of Funeral Expense Insurance Policies

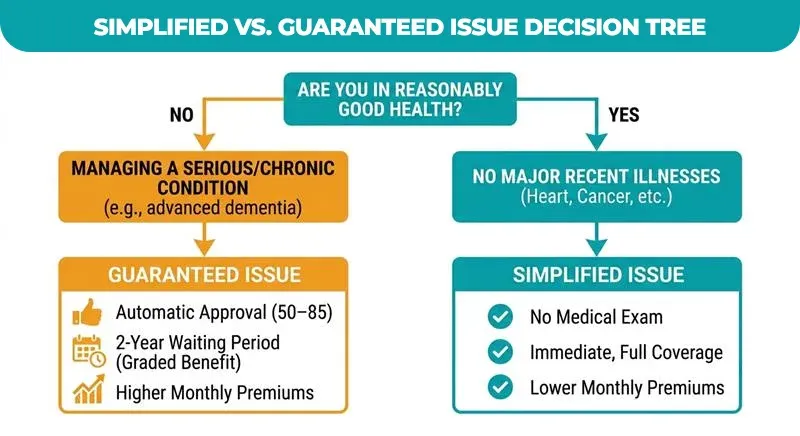

Not every applicant qualifies for the same product. Which type of insurance policy for funeral expenses fits you comes down mostly to your current health.

Simplified Issue Whole Life

This is the most common form of final expense funeral insurance. The application asks a handful of yes/no health questions about conditions like heart disease, cancer, or recent hospitalizations, but requires no blood work, no urine sample, and no physical exam. Applicants in reasonably good health are typically approved within days and gain immediate, full coverage.

Guaranteed Issue Whole Life

Guaranteed issue policies ask no health questions at all and require no exam; approval is automatic for anyone within the eligible age range (commonly 50-85). This makes it the only path to coverage for people with serious health conditions, including advanced dementia or Alzheimer’s, who have been declined elsewhere. The insured must still personally apply and consent to the policy; a power of attorney generally cannot complete this step on someone else’s behalf once they can no longer understand and sign for themselves.

| The catch waiting periods: guaranteed issue policies carry a standard two-year waiting period (also called a graded death benefit). If the insured dies of natural causes within that window, the insurer does not pay the full face value; it refunds the premiums paid, typically plus 10% interest. After two years, the policy pays the complete death benefit for any cause of death. |

How Much Does Funeral Expense Insurance Cost?

Premiums for life insurance to cover funeral expenses are calculated from four main variables: your age at application, your gender, the coverage amount you choose, and whether you use tobacco. Because women statistically outlive men, female applicants generally pay noticeably less per month than male applicants of the same age for identical coverage.

Sample Monthly Premiums for $10,000 in Coverage

| Age | Female (approx.) | Male (approx.) |

| 50 | $30 – $45 | $35 – $50 |

| 60 | $35 – $50 | $42 – $58 |

| 65 | $41 – $45 | $54 – $58 |

| 70 | $45 – $60 | $58 – $75 |

| 75 | $55 – $71 | $70 – $97 |

| 80 | $70 – $90 | $95 – $148 |

Guaranteed issue policies run roughly 25-40% higher per dollar of coverage than simplified issue policies, since the insurer is accepting risk with zero health information. Nicotine use can add a similar surcharge on either product type.

Is Funeral Expense Insurance Worth It For You?

Who It’s Best For

- Seniors over 60 who want a fixed, predictable line item instead of leaving costs to whoever survives them.

- Anyone with a minor health condition that disqualifies them from traditional term or standard whole life insurance.

- People without $10,000-$15,000 in liquid, earmarked savings set aside specifically for end-of-life costs.

Who Should Consider Skipping It

- Younger applicants in excellent health, who will usually get far more coverage per dollar from a standard term or whole life policy.

- Anyone who already has a fully funded, liquid estate or an existing life insurance policy large enough to absorb funeral costs.

How to Choose the Best Funeral Insurance Plan

Price Out Your Actual Plans

Decide roughly whether you want burial or cremation, with or without a service, and use the cost tables above as a starting benchmark for your region. This tells you what face amount you actually need rather than guessing.

Shop Multiple Carriers

Rates for identical coverage can vary by 30% or more between insurers for the same age and health profile. Heavily advertised television and direct-mail offers are frequently priced well above what an independent agent can find you across a panel of carriers.

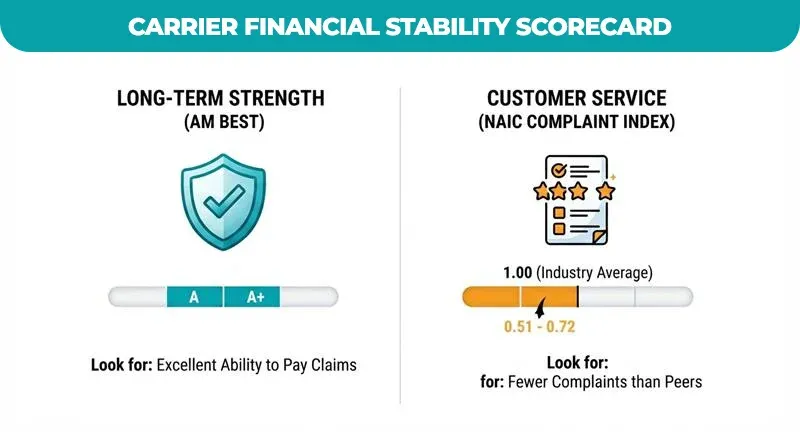

Vet the Carrier’s Financial Stability

Two numbers matter more than the sales pitch:

- AM Best rating: measures the insurer’s financial strength and ability to pay claims decades from now. Look for A or A+ ratings.

- NAIC complaint index: The industry average complaint volume in relation to market share is represented by a score of 1.00; scores significantly below 1.00 (some reputable final expense carriers record indexes as low as 0.51-0.72) indicate fewer customer complaints than peers, while indexes climbing toward 3-4x the baseline are a signal to look closer before buying.

Conclusion

Funeral expense insurance isn’t about dwelling on a somber day or focusing on an unhappy event; rather, it represents a deeply considerate and profoundly practical act of care for the people who matter most to you. By putting a dedicated policy in place, you establish an ironclad financial safety net that ensures your grieving family can focus entirely on honoring your memory and celebrating your life, rather than being forced to frantically scramble during an already devastating week to cover an unexpected out-of-pocket bill that routinely runs upwards of $8,000 to $10,000.

A modest, predictable monthly premium locked in today is the single strongest shield standing between your loved ones and the intense financial stress of modern end-of-life costs. Because final expense insurance rates are strictly calculated based on your age at the exact time of your application, your premiums will never be lower than they are right now.