Introduction

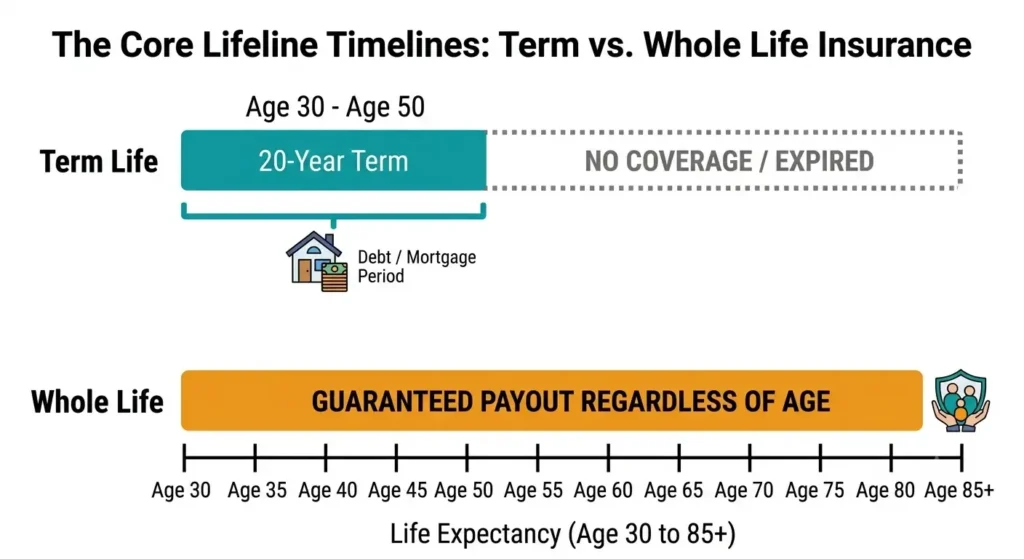

Term life insurance is temporary, low-cost coverage that pays a death benefit only if you die within a set period, usually 10 to 30 years. Whole life insurance is permanent coverage that lasts your entire life and builds a cash value account, but it typically costs five to fifteen times more for the same payout. For most young families, paying off a mortgage term is the practical choice. For estate planning or a lifelong dependent, whole life earns its higher price tag.

Insurance shopping shouldn’t feel like reading a map in a storm, but the jargon, the sales pitches, and the conflicting advice from well-meaning relatives make it feel that way. Roughly 102 million American adults are uninsured or underinsured, according to LIMRA’s Insurance Barometer research, and a big chunk of that gap comes down to confusion over which policy type actually fits their life.

What Is Term Life Insurance?

Term life insurance can be compared to apartment rentals. You pay a monthly premium for a fixed window of coverage, and if you pass away during that window, your beneficiaries receive a tax-free lump sum. If the term ends and you’re still alive, the policy simply expires. No refund, no leftover value, but also no wasted overhead while you had it.

That simplicity is exactly why term life insurance vs whole life insurance comparisons so often tilt toward term for younger buyers. A healthy 30-year-old can typically lock in a $500,000, 20-year term policy for somewhere in the $20 to $30 a month range, according to multiple carrier quote averages. That’s less than most people spend on streaming subscriptions, for coverage that could replace a decade of lost income.

Where term life insurance earns its reputation:

- The death benefit is only a straightforward, tax-free payout to your beneficiaries

- Premiums stay level for the entire term on most policies

- Coverage amounts scale easily to match a mortgage balance or income-replacement need

- Many term policies convert to permanent coverage later, without a new medical exam

What Is Whole Life Insurance?

Whole life insurance works more like buying a house instead of renting it. Coverage lasts for your entire life as long as you keep paying premiums, and part of every payment funds a cash value account that grows on a tax-deferred basis. You can eventually borrow against that cash value or withdraw from it, which is the feature insurance agents lean on hardest when pitching whole vs term life insurance to older or wealthier clients.

The catch is cost. Whole life premiums for the same death benefit typically run five to fifteen times higher than a comparable term policy, since you’re funding a lifetime guarantee plus a savings component rather than renting protection for a season of life. That premium gap is the single biggest reason the term insurance vs whole life insurance debate gets so heated among financial advisors.

Where whole life insurance earns its keep:

- As long as premiums are paid, coverage is perpetual.

- Cash value grows tax-deferred and can be borrowed against for emergencies or opportunities

- Premiums are typically fixed for life, with no re-underwriting as you age

- Some policies pay annual dividends that can offset future premiums

Term vs Whole Life Insurance: Head-to-Head Comparison

Here’s the whole life vs term life insurance decision boiled down to one table so you can scan the facts instead of hunting for them in paragraphs.

| Feature | Term Life Insurance | Whole Life Insurance |

| Coverage period | Set years (10, 20, or 30) | For the duration of your life, provided that premiums are paid |

| Premium cost | Low, usually fixed for the term | For the same death benefit, five to fifteen times more |

| Cash value | None | Grows on a tax-deferred basis; can be borrowed against |

| Complexity | Simple pay, die, or outlive it | Moderate to high, with riders and dividend options |

| Best for | Income replacement, mortgages, young families | Estate planning, lifelong dependents, high net worth |

Pros and Cons: Weighing Your Options

Term Life Insurance: Pros and Cons

- Pro: Exceptionally budget-friendly, which frees up cash to invest elsewhere

- Pro: Coverage amount is easy to right-size to a specific debt or income-replacement goal

- Con: No equity builds up to outlive the term, and you walk away with nothing

- Con: Renewing after the term ends gets expensive fast, since pricing resets to your current age

Whole Life Insurance: Pros and Cons

- Pro: Permanent protection with a guaranteed payout, regardless of when you die

- Pro: Predictable, tax-deferred cash growth that can double as a financial backstop

- Con: Premiums are rigid and expensive, which strains budgets during lean years

- Con: Early cash value growth is slow, since fees and commissions eat into the first several years of payments

Most consumers are unaware of how important that final element is. Industry termination data shows individual life policies lapse at a rate of roughly 8.5% per year by policy count, and whole life policies are disproportionately represented in early lapses because the premium burden catches people off guard. A policy you can’t afford to keep isn’t protecting anyone.

Why Dave Ramsey (and Many Financial Advisors) Push Back on Whole Life

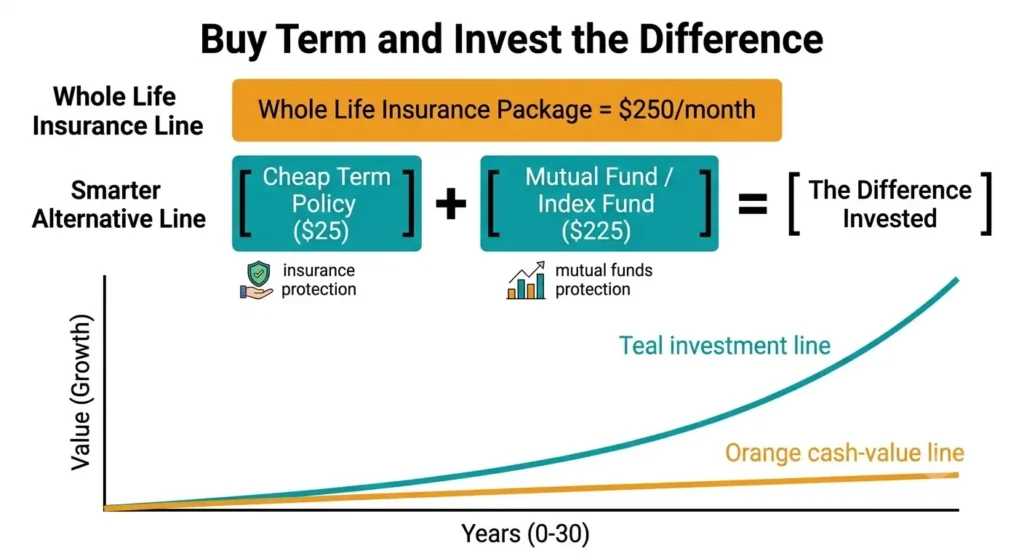

Search “Dave Ramsey whole vs term life insurance,” and you’ll find a consistent message: buy term, invest the difference. Ramsey’s argument isn’t that whole life insurance is a scam; it’s that bundling insurance with a mediocre savings vehicle usually underperforms simply buying cheap term coverage and putting the premium savings into an index fund or retirement account.

The math behind this view is straightforward. If a $500,000 whole life policy costs $250 a month and the equivalent term policy costs $25, that $225 monthly difference invested consistently in a diversified portfolio over 20 to 30 years tends to outgrow the guaranteed returns baked into most whole life cash value accounts. That said, this strategy only works if the person actually invests the difference instead of spending it, which is the part critics of “buy term and invest the difference” point out most often.

How to Choose: Term or Whole Life for Your Situation

Neither policy is universally right or wrong. The better question is which one matches your actual financial timeline.

Choose Term Life Insurance If:

- You have a 25- or 30-year mortgage and want coverage that matches the loan payoff schedule

- You’re raising young kids and need to replace your income through their launch into adulthood

- You’d rather invest the premium savings yourself than pay for a bundled savings account

- Your coverage need is temporary, a specific debt, a specific number of working years, or a specific goal

Choose Whole Life Insurance If:

- You have a lifelong dependent, such as a child with special needs, who will require support after you’re gone

- You’re using it as one piece of an estate plan to help cover eventual estate taxes

- You’re a high-net-worth individual who has already maxed out 401(k) and IRA contributions and wants another tax-advantaged vehicle.

- You want absolute certainty that a payout happens no matter when you die, and you can comfortably afford the premium for decades.

Conclusion

Choosing between term and whole life insurance is never a one-size-fits-all battle; it is about matching a policy structure directly to your personal financial roadmap. For families looking to replace temporary income or safeguard a mortgage, budget-friendly term life insurance provides an absolute, straightforward safety net without any wasted overhead. However, if your wealth strategy requires permanent protection for estate planning or a lifelong dependent, whole life insurance delivers a guaranteed lifelong payout that justifies its higher premium cost.

Stop letting confusion leave your loved ones exposed to a devastating financial gap. Take a fearless, definitive step today by calculating your precise coverage needs using the proven rule of thumb of 10 to 12 times your annual income. Armed with that number, bypass the generic sales scripts, request tailored quotes from highly respected A.M. Best-rated carriers, and claim bulletproof peace of mind for your family’s future.

Ready to Secure Your Family’s Financial Future?

Don’t navigate the insurance storm alone. Whether you need the laser-focused affordability of a term policy or the lifelong security of whole life coverage, Premier Services Agency does the heavy lifting for you. We compare top-rated carriers to find the bulletproof coverage your family deserves at a price that fits your budget. Click Here to Get Your Free, No-Obligation Quote.