Introduction

Planning for end-of-life costs is stressful enough without wading through confusing insurance ads. Between funeral bills, outstanding medical debt, and the fear of burdening family members, it’s no surprise that low-premium commercials, the ones promising coverage for “just pennies a day,” catch attention fast.

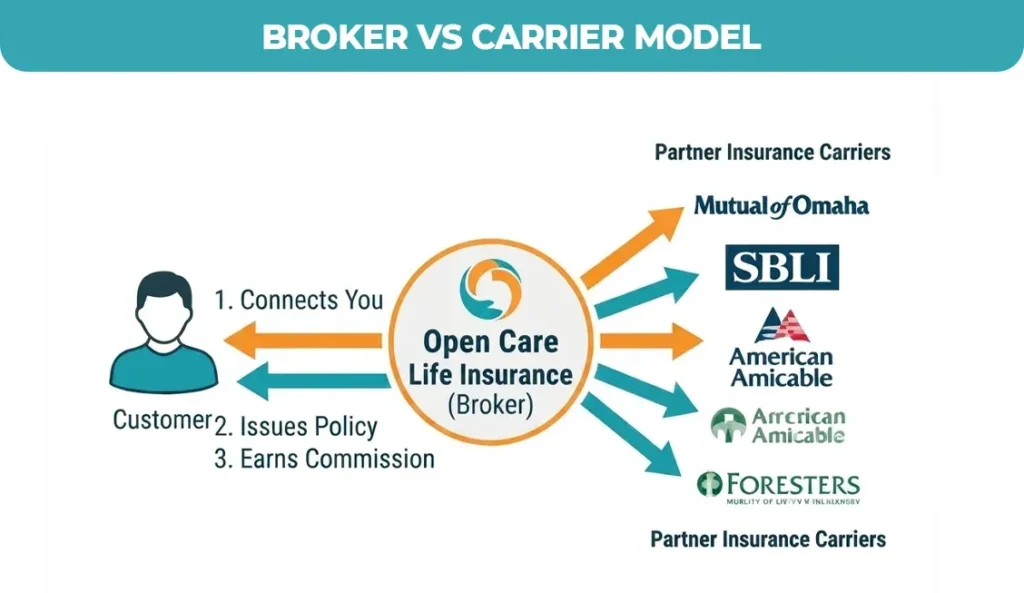

Open Care life insurance is one of the most visible names in that space. But before you request a quote, it’s worth understanding what you’re actually signing up for. Open Care Seniors (also marketed as “Open Care Senior Plan”) is an independent insurance brokerage, not a licensed insurance carrier. It doesn’t underwrite policies, set final premiums, or pay claims itself; it connects you with one of several partner insurance companies that do.

This article demystifies what Open Care life insurance is, how its plans work, where the pricing gets misleading, and how to shop smarter so you don’t overpay for a policy that’s supposed to protect your family, not create more financial stress.

What Is Open Care Life Insurance?

Open Care Life Insurance operates as an independent brokerage that aggregates what it calls “Senior Care Plans,” final expense, and burial insurance products sold on behalf of other carriers.

Agency vs. insurer. When you apply through Open Care, the policy that’s actually issued comes from a third-party insurance company. Industry reviewers have identified partners such as Mutual of Omaha, American Amicable, SBLI, and Foresters, though Open Care does not publish a full list of its carrier network on its website or in its commercials.

Target demographic. Open Care’s marketing is built around adults roughly 50 to 85 years old, with some materials suggesting eligibility as young as 18 for term products and as old as 90 for certain final expense plans.

Business model. As a broker, Open Care Life Insurance earns commissions from the carriers it places business with, not from underwriting policies directly. This is a legitimate and common structure in the insurance industry (many “senior life insurance” brands operate the same way), but it means the burden of comparison-shopping falls on you, since a broker isn’t obligated to show you every option on the market.

One important note for anyone researching this company online: a separate, unrelated business also uses the name “Opencare,” a dental-referral platform based in San Francisco with its own Better Business Bureau profile and complaint history. That company has nothing to do with life insurance.

Understanding “Open Care Senior Plans” and Coverage Types

Final expense (burial) insurance is the core product. These are small whole life policies, typically ranging from $2,000 to $50,000 in death benefit, designed to cover funeral costs, cremation, outstanding medical bills, or small debts, not to replace income or build significant wealth for heirs.

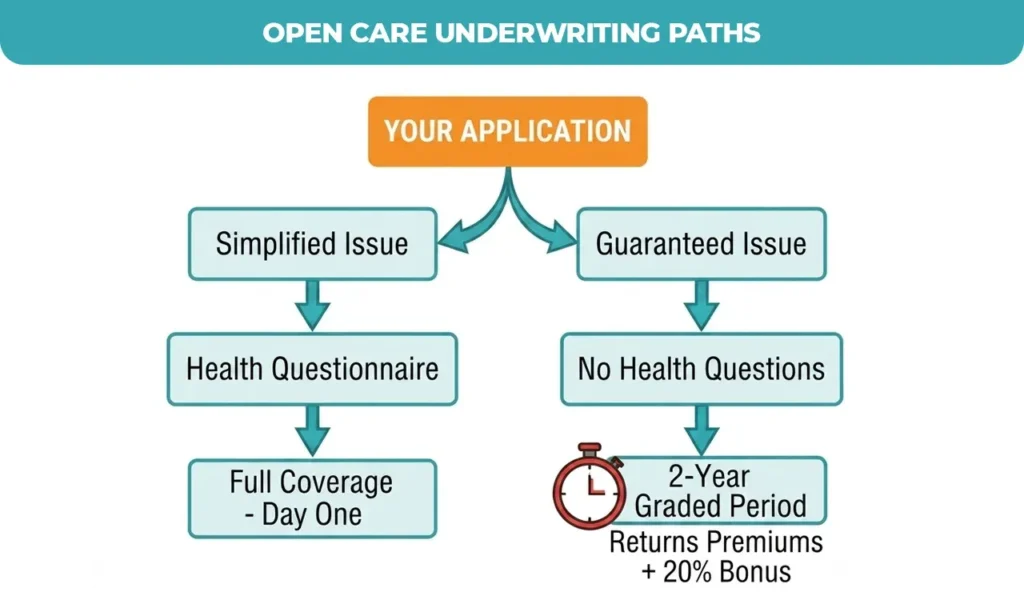

Open Care life insurance offers two main underwriting paths:

- Simplified Issue: No medical exam is required, but you must answer a health questionnaire. Applicants who qualify get day-one, full coverage (assuming no misrepresentation on the application).

- Guaranteed Issue: No health questions and no medical exam approval is close to automatic. The tradeoff is a two-year graded (waiting) period: if the policyholder dies of natural causes within the first 24 months, beneficiaries typically receive only a refund of premiums paid plus interest, not the full face amount. Accidental death is usually covered at 100% from day one.

Term life insurance is also available through Open Care, generally in amounts from $25,000 up to $500,000–$1,000,000, in 10-, 20-, or 30-year terms for applicants up to around age 75. Term life requires full health underwriting, so it’s less accessible for many seniors and isn’t the focus of Open Care’s television marketing, as the final expense is.

The Truth About Costs: Beyond the “$7.49/Month” Ads

Open Care life insurance advertising leans hard on a teaser rate: policies “starting at $7.49 per month.” In practice, that figure represents the cheapest possible combination of variables: the smallest coverage amount ($2,000), the youngest eligible age (around 50), a non-smoker, in excellent health, and often female (women typically get lower life insurance rates than men of the same age).

What actually moves your price:

- Age premiums rise steadily the older you are at application, since final expense policies are priced to be paid up over your remaining life expectancy.

- Gender and smoking status, non-smoking women generally get the lowest rates; smokers pay significantly more regardless of gender.

- Health history even simplifies issue plans. Use your answers to a health questionnaire to sort yourself into a rate class (preferred, standard, or substandard).

- The death benefit amount of a $25,000 policy costs meaningfully more per month than a $10,000 policy at the same age and health class.

Approximate Monthly Cost by Age $10,000 Simplified Issue Policy, Non-Smoker

| Age | Approximate Monthly Premium |

| 50 | $15 – $25 |

| 60 | $30 – $50 |

| 70 | $50 – $85 |

| 80 | $85 – $150+ |

The common pitfall I see people make with any “as low as” insurance ad, not just Open Care’s, is anchoring on the headline number and then feeling blindsided. The real quote is three or four times more expensive. That’s not necessarily deceptive pricing in a legal sense (the $7.49 rate is real, for that one specific buyer profile), but it is a marketing tactic designed to get the phone to ring. Always ask for your specific quote in writing before you commit to anything.

Pros and Cons: A Balanced View

Pros

- Streamlined application, many quotes can be completed over a short phone call.

- No medical exam required for simplified issue and guaranteed issue plans.

- Accessible to applicants with pre-existing conditions who might be declined elsewhere.

- Access to multiple carrier products through one point of contact.

Cons

- Lack of carrier transparency. You often won’t learn which insurance company is actually underwriting your policy and therefore can’t check that carrier’s financial strength rating (A.M. Best) or BBB standing until late in the process.

- Marketing-heavy approach. Reviewers and complaint boards consistently flag a high volume of follow-up calls and mailers after a quote request, sometimes multiple contacts per week.

- Potential for overpayment. Because Open Care life insurance doesn’t publicly disclose or compare its full carrier list, you can’t be certain it’s shopping the entire market on your behalf. Comparing independently is the only way to know you’re getting a competitive rate.

How to Shop for Final Expense Insurance Like a Pro

- Calculate what you actually need. Look up average funeral and burial costs in your area (nationally, these commonly fall between $8,000 and $12,000) and size your coverage to that number rather than to a round figure that sounds appealing.

- Get quotes from at least three sources: a broker like Open Care Life Insurance, a direct carrier such as Mutual of Omaha or Aetna, and an independent agent who represents multiple A-rated companies.

- Ask directly: “Which insurance company is underwriting this policy?” A legitimate agent should answer immediately. Hesitation or vague answers are a warning sign.

- Check the named carrier’s financial strength rating through A.M. It is best to verify the carrier’s BBB profile rather than the broker’s before signing any documents.

Red flags to watch for:

- A company that refuses to name the underwriting insurer before you apply.

- High-pressure tactics, same-day-only pricing, repeated auto-dialed calls, or urgency language designed to prevent comparison shopping.

- Long waiting periods are offered by default, even to applicants in reasonably good health who could likely qualify for immediate full coverage elsewhere.

Conclusion

Open Care life insurance offers a convenient, one-stop-shop experience for seniors who want final expense coverage without a medical exam. That convenience is real, but so is the gap between the advertised “starting at” price and what most people actually pay. Because Open Care life insurance doesn’t disclose its carrier network upfront, the responsibility for verifying transparency and financial strength falls on you.

Before you commit to any final expense policy through Open Care life insurance or any other broker, get your specific quote in writing, confirm the name of the underwriting carrier, and compare it against at least two other sources. A few extra phone calls now is a small price to pay for making sure your family is protected by a policy you can actually trust.

Stop Guessing with Your Coverage

Tired of confusing marketing tactics and hidden carrier details? At Premier Services Agency, we believe in full transparency. We shop the market for you, naming the exact carriers we work with so you can verify their financial strength before you sign.