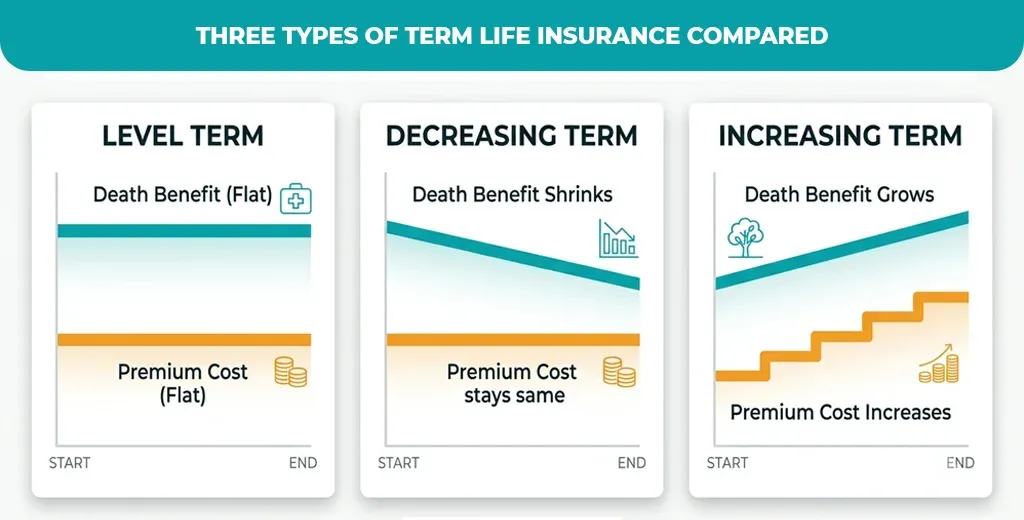

Level Term vs. Decreasing and Increasing Term Life Insurance

When people search “term level life insurance” or “term life insurance level,” they’re usually trying to distinguish level term from its two structural cousins. Here’s the side-by-side:

| Policy Type | Premium | Death Benefit | Best Used For |

| Level Term | Fixed for the full term | Fixed for the full term | Income replacement, general family protection |

| Decreasing Term | Usually fixed | Shrinks on a set schedule | Paying off a mortgage or amortizing loan |

| Increasing Term | Rises over time | Grows over time | Hedging long-term inflation risk |

For the vast majority of buyers, replacing income, covering a family’s living costs, or protecting against the unexpected level term is the more useful default. Decreasing term only makes sense when your liability itself is decreasing (a mortgage payoff schedule, for example); tying your family’s protection to a shrinking number is rarely the right call for open-ended needs like raising kids or replacing a salary.

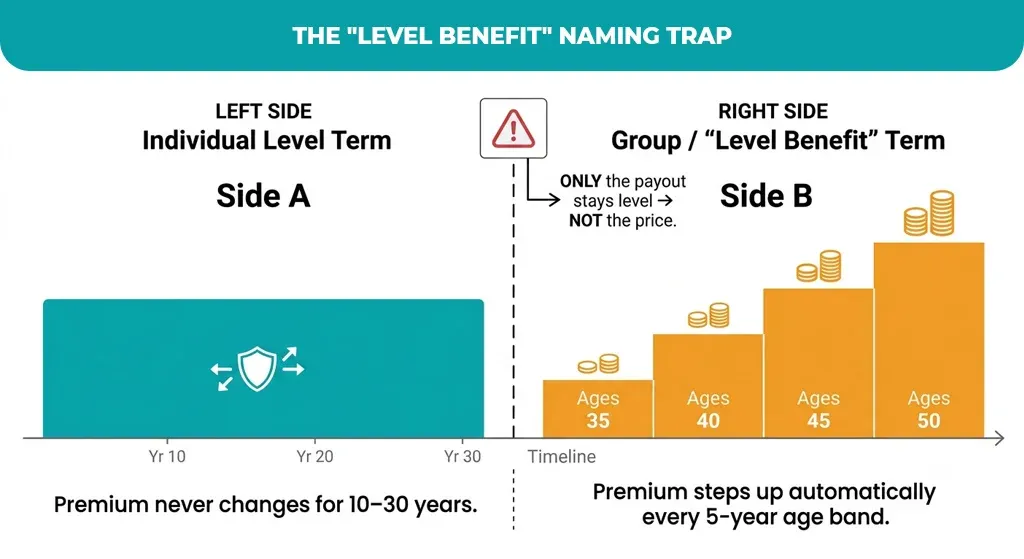

Individual Level Term vs. “Level Benefit” Term: A Naming Trap Worth Knowing

This is the category’s most frequent source of confusion, and since it has an impact on actual money, it’s important to be exact. Individual level term life insurance, the kind underwritten directly to you based on your age, health, and a medical exam or health questionnaire, locks both the premium and the benefit for the entire term you select.

Group and association-branded products, including some AARP-endorsed level benefit term life insurance plans issued through New York Life, work differently. In those plans, the death benefit stays level, but the premium is not guaranteed for the full duration; it rises as you move into a new five-year age band. That’s a meaningfully different product from individually underwritten level term insurance, even though the word “level” appears in both names.

Level Term Life Insurance Rates: What Drives the Price

A healthy 35-year-old can often secure a 20-year, $250,000 level term policy for under $20 a month with a preferred health rating, a figure that’s remained a reliable industry benchmark for years. But the specific number moves on a few dependable levers:

- Age at purchase. Insurers price in five- to ten-year bands based on statistical mortality tables. Waiting five years to buy typically costs more than the five years of protection you saved by delaying.

- Health classification. Preferred-plus, preferred, standard, and substandard tiers can create a multiple-fold difference in premium for identical coverage amounts.

- Term length. Locking a rate for 30 years costs more per month than 15 years, because the insurer is guaranteeing that price for twice as long, but the per-year cost of certainty is usually worth it if your income-replacement need genuinely spans that long.

| Term Length | Typical Buyer Profile | Common Reasons to Choose It |

| 15-Year Level Term | Buyers 10–15 years from a mortgage payoff or a fixed financial deadline | Matches a shorter, known obligation at the lowest possible premium |

| 20-Year Level Term | Parents of young children, most first-time buyers | Covers the working years until kids are financially independent |

| 30-Year Level Term | Younger buyers, new homeowners, longer income-replacement horizons | Locks a rate for the longest stretch while health and age are favorable |

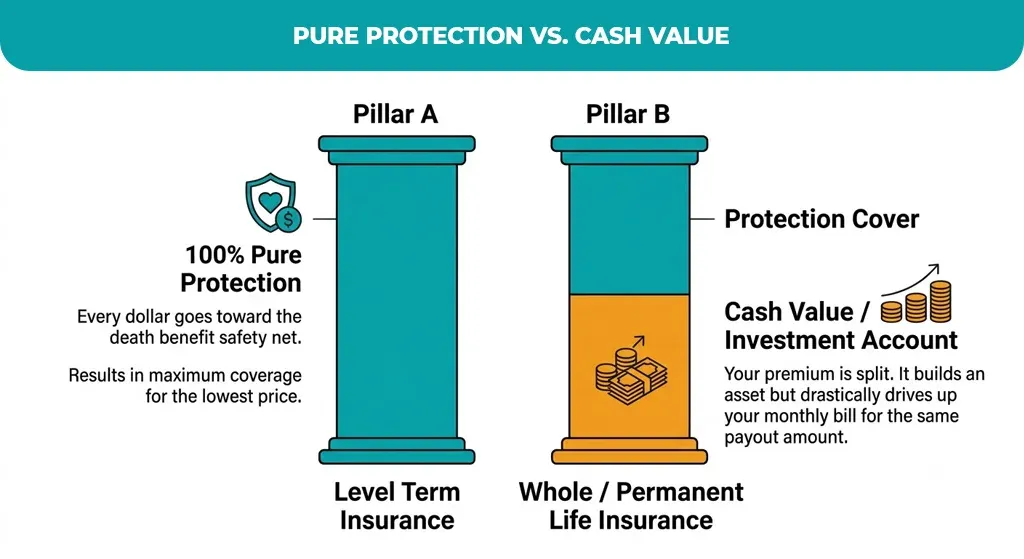

Benefits and Drawbacks of Level Term Life Insurance

Benefits

- Predictable budgeting. Ten, twenty, or thirty years of the exact same bill is easy to plan around.

- Maximum coverage per premium dollar. Because there’s no cash value subsidizing the price, you can typically buy several times more coverage per dollar than with permanent insurance.

- Tax-free payout. In the U.S., death benefits are generally received income-tax-free by beneficiaries.

Drawbacks

- No payout if you outlive it. If you outlive the term, you get nothing back for the premiums paid; the coverage simply expires.

- Steep renewal costs. Once the level period ends, renewing without new underwriting is usually far more expensive than the original rate.

- No cash value. Unlike whole life, there’s no savings or loan feature to tap into later.

These disadvantages of term life insurance aren’t unique to the level structure; they’re inherent to term insurance generally. The tradeoff is the same one you make with car or home insurance: you’re paying for protection against a risk, not building an asset, and that’s exactly what keeps the price so low.

Customizing a Level Term Policy with Riders

A level term life insurance policy is intentionally simple, but a handful of optional riders let you adapt it to real-life curveballs:

- Waiver of Premium Rider: Suspends your premium obligation if you become seriously injured or disabled and lose your income, without lapsing the policy.

- Accelerated Death Benefit Rider lets you access a portion of the death benefit early if you’re diagnosed with a qualifying terminal illness.

- The Term Conversion Rider lets you convert some or all of your term coverage into a permanent policy later, typically without a new medical exam, the single most important safety valve in the entire product.

- Child or Spousal Term Rider adds a smaller amount of coverage for a spouse or children under the primary policy.

Conclusion

Level term life insurance cuts through the noise of complex financial products by offering an ironclad, predictable promise. For a single, unmoving price, you secure a reliable safety net tailored precisely to the span of your family’s most critical financial milestones. It serves as a straightforward, budget-friendly shield designed to protect your household from the unexpected.

Don’t wait for a milestone birthday or an unexpected health change to drive your premiums up. Taking action today allows you to compare competitive quotes and lock in low rates while time and health are on your side. Secure your family’s financial legacy now so you can focus on the present with genuine peace of mind.