Inroduction

Most families do not have $10,000 in a dedicated fund waiting for this exact expense. Credit cards, personal loans, or GoFundMe pages fill the gap instead, and that financial strain often outlasts the grief itself. A burial insurance policy, also called final expense insurance, exists specifically to close this gap. It is a small, simplified whole life policy built to cover funeral services, cremation, burial plots, and related end-of-life costs without requiring a medical exam.

This guide breaks down exactly how a burial insurance policy works, the different types of coverage on the market, how it compares to traditional life insurance, and how to choose a policy that will not let your family down when it matters most.

What Is a Burial Insurance Policy?

Burial insurance is a subset of whole life insurance, which means the coverage never expires as long as premiums are paid; there is no annual renewal or age cutoff that cancels the policy. It also builds modest cash value over time, unlike a term policy that pays nothing if the insured outlives the term.

The defining characteristic of burial insurance is accessibility. Because policies are issued at low face values, insurers can afford to skip the invasive underwriting used for larger life insurance policies. Upon the policyholder’s death, the insurer pays a lump-sum death benefit directly to the named beneficiary, who has full control over how the money is spent.

How Does a Burial Insurance Policy Work?

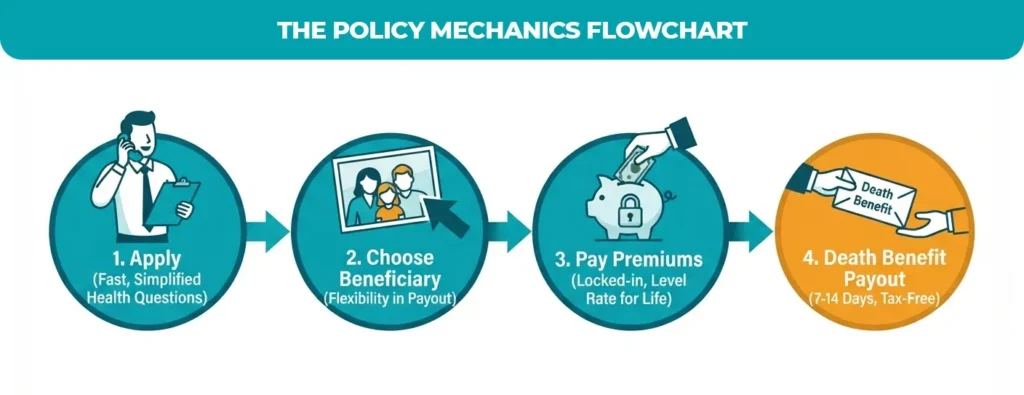

The mechanics are intentionally simple compared to larger life insurance products:

- Apply. Complete a short application, often over the phone in 15-20 minutes, answering basic health and lifestyle questions.

- Choose a beneficiary. Name one or more people who will receive the payout. This does not have to be a funeral home.

- Pay premiums. Premiums are locked at the rate you qualify for on day one and do not rise as you age or if your health declines.

- Death benefit payout. Upon death, the beneficiary files a claim with a copy of the death certificate, and the insurer typically pays out within 7-14 business days.

Unlike a pre-need funeral plan, the death benefit here is not restricted to one funeral insurance or one line-item expense. Beneficiaries can use the funds for cremation, a traditional burial, outstanding medical bills, credit card debt, or simply living expenses while the estate is settled.

Types of Burial Insurance Coverage

Simplified issue policies ask a handful of health questions and generally exclude applicants with serious conditions like recent cancer treatment or a terminal diagnosis, but approval is fast, and full benefits apply immediately.

Guaranteed issue policies accept virtually every applicant within the eligible age range, usually 50 to 85, regardless of health history. The tradeoff is a graded death benefit: if the policyholder dies of natural causes within the first two to three years, beneficiaries typically receive only a refund of premiums paid plus interest, not the full face value.

| Coverage Type | Pros | Cons | Best For |

| Simplified Issue | Faster approval (24-48 hrs); moderate premiums; full benefit from day one if approved | A health questionnaire can trigger denial for major conditions | Seniors in average-to-good health |

| Guaranteed Issue | No health questions or exam; near-instant acceptance | Highest premiums per dollar of coverage; 2-3 year graded waiting period | Applicants with serious pre-existing conditions |

| Pre-Need Insurance | Locks in today’s funeral prices with a specific home | Not portable; funds tied to one funeral provider | Those who have already chosen a funeral home |

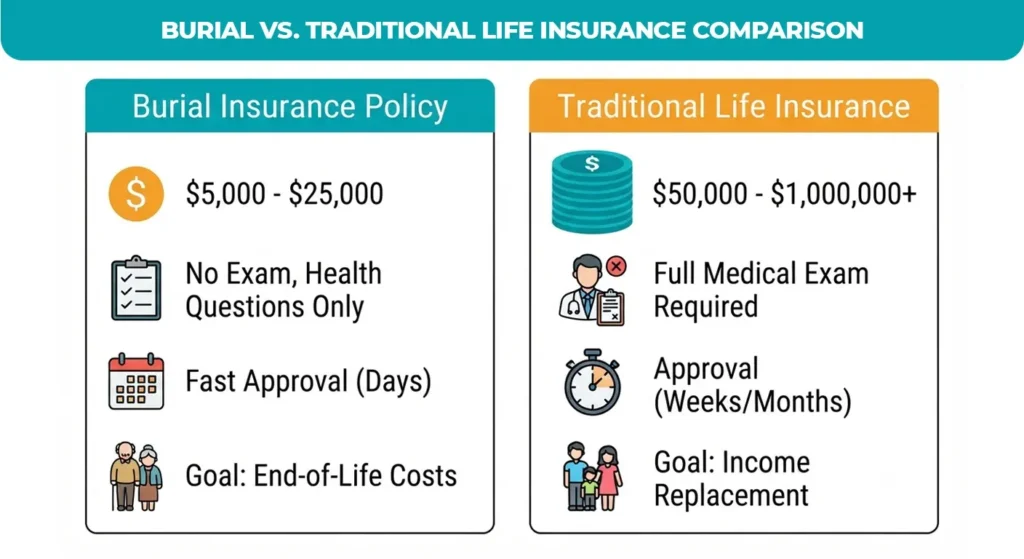

Burial Insurance vs. Traditional Life Insurance

The National Funeral Directors Association (NFDA) has tracked steadily rising funeral costs for over a decade, citing increases in casket, vault, and service fees that consistently outpace general inflation. That trend is the core justification for a dedicated final expense product: a policy sized specifically for a cost category that keeps climbing, rather than relying on a general-purpose life insurance policy that may not exist at all for older applicants.

| Feature | Burial Insurance Policy | Traditional Life Insurance |

| Coverage Amount | $5,000 – $25,000 | $50,000 – $1,000,000+ |

| Underwriting | None too simplified; health questions only | A full medical exam is typically required |

| Approval Speed | Days | Weeks to months |

| Primary Goal | Cover end-of-life costs | Income replacement and estate protection |

| Typical Buyer Age | 50-85 | 20-65 |

For younger, healthier applicants who still need income replacement for a spouse or children, a traditional term or whole life policy is usually the more efficient way to buy a large death benefit. Burial insurance becomes the more practical option once age or health conditions make traditional underwriting difficult or prohibitively expensive.

Is a Burial Insurance Policy Right for You?

Use this checklist to evaluate your own situation:

- Do you have at least $10,000-$15,000 set aside specifically for funeral costs?

- Would your family need to take on debt to cover your final expenses today?

- Do you have an existing life insurance policy that your family knows about and can access quickly?

- Are you between the ages of 50 and 85 with no plans to purchase more extensive traditional coverage?

- Do you have health conditions that would make traditional underwriting difficult or expensive?

Answering ‘no’ to the savings and existing-coverage questions, combined with a ‘yes’ to any of the health or age questions, is a strong signal that a dedicated burial policy is worth pricing out.

Tips for Selecting the Best Policy

In decades to come, a policy will only be as good as the organization supporting it. Check the insurer’s AM Best rating. Generally, an A- or higher rating is considered financially sound for a company that may need to pay a claim 20 or 30 years after issuance.

Request quotes from multiple carriers rather than accepting the first offer from a single agent. Face amount, premium, and waiting-period terms can vary significantly between insurers for the exact same health profile.

Read the policy’s fine print specifically for two terms: ‘graded benefit’ and ‘waiting period.’ These clauses determine whether your family receives the full face value or only a refund of premiums if death occurs in the early years of the policy.

Finally, get written confirmation that the premium is level for life. Some older or poorly structured policies allow premium increases at set age thresholds, a detail that defeats the purpose of a fixed-cost final expense plan.

Conclusion

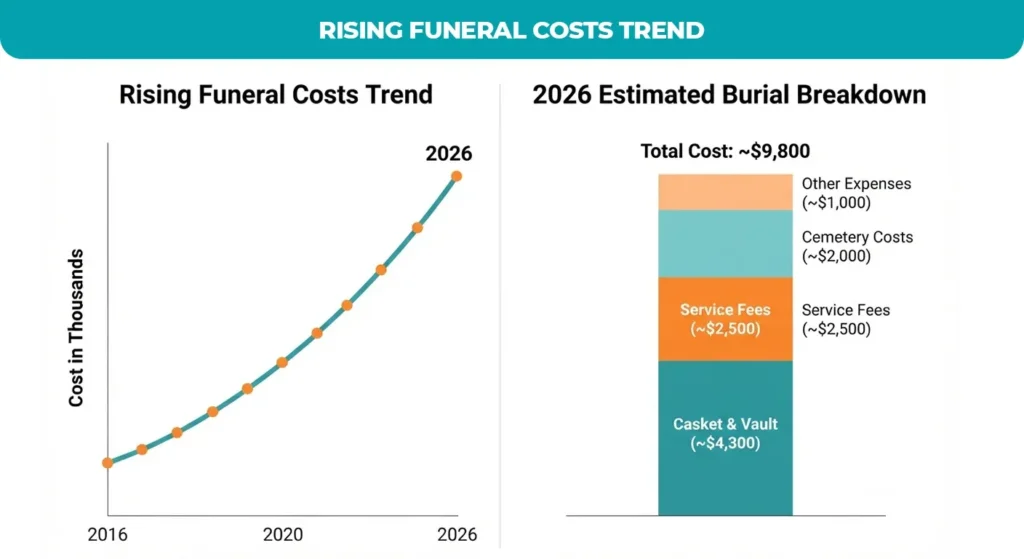

A burial insurance policy is not a purchase most people look forward to making, but it remains one of the most effective ways to secure peace of mind for your loved ones. By removing a rising financial burden, which now averages between $8,300 and $9,995 for a traditional burial with a vault in 2026, you ensure your family can focus on grieving rather than managing unexpected debt.

If you find that your current savings are insufficient, request quotes from at least three A-rated insurers before your next birthday, as premiums are locked in at your age of application. Ready to take the next step? Reach out to a licensed final expense advisor today to lock in a fixed, affordable rate while you still qualify for the best pricing tier.

Ready to protect your family’s future?

Don’t leave your loved ones with the burden of funeral debt. Premier Services Agency specializes in helping seniors secure affordable, fixed-rate coverage that lasts a lifetime. Reach out to our licensed final expense advisors today for a free, no-obligation quote and lock in your rate before your next birthday.