Introduction

Few financial conversations carry as much quiet anxiety as life insurance. For millions of older adults and people managing chronic health conditions, the fear isn’t death itself, it’s rejection. A denied application, a rated policy with sky-high premiums, or a battery of medical exams that feel invasive at best and disqualifying at worst. Guaranteed life insurance exists precisely to remove that fear. It offers a path to coverage where acceptance is not a question, only a formality.

Guaranteed life insurance, sometimes called guaranteed issue life insurance or guaranteed acceptance life insurance, is a category of permanent life insurance that eliminates medical underwriting. There are no exams, no blood tests, and in most cases, no health questions at all. Approval is based on age and state of residence, not medical history.

This guide walks through what guaranteed life insurance is, who actually benefits from it, how the policies work mechanically (including the often-misunderstood graded death benefit), and a clear-eyed look at the pros and cons so you can make an informed decision rather than a fear-driven one.

What Is Guaranteed Issue Life Insurance?

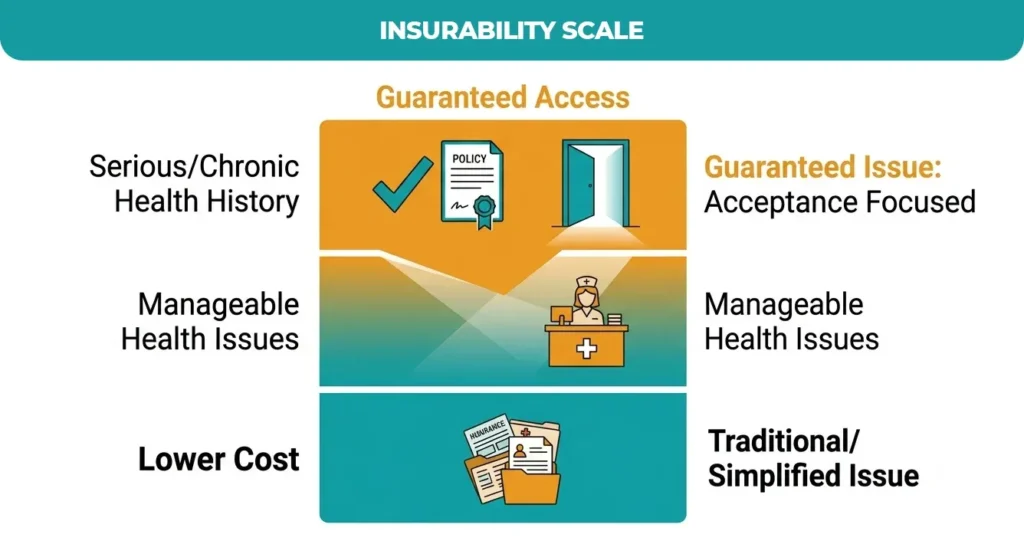

Guaranteed issue life insurance is a type of permanent, guaranteed whole life insurance policy that approves every applicant within an eligible age range, typically 50 to 85, without medical exams, lab work, or health questionnaires. Coverage and premiums are fixed for life as long as the policy is described as guaranteed whole life insurance rather than a guaranteed term life insurance product, which is far less common.

What does ‘guaranteed issue’ actually mean?

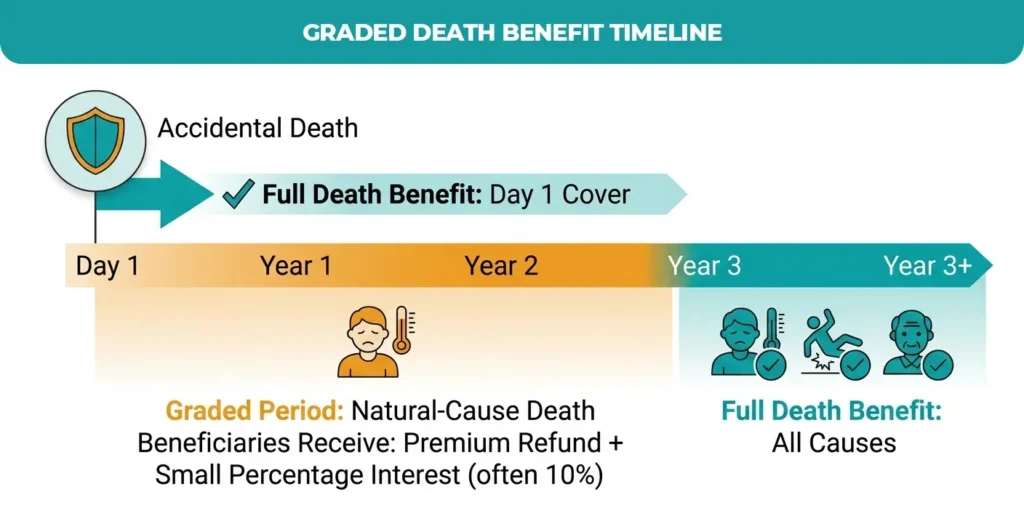

“Guaranteed issue” (sometimes marketed as guaranteed acceptance whole life insurance) means the insurer cannot decline you based on health. In our professional experience, this is the single most misunderstood feature of the product: guaranteed approval applies to whether you get a policy, not to how much the death benefit pays out immediately, a distinction the graded death benefit section below addresses directly.

Why do insurers offer this product?

Insurers offer guaranteed acceptance life insurance, no health questions products, as a deliberate trade-off. Because the carrier has no medical data on the applicant, it cannot price risk individually. Instead, it manages risk at the portfolio level by capping coverage amounts, charging higher premiums per thousand dollars of coverage, and building in a graded benefit period. Data suggests that this structure lets carriers like Mutual of Omaha, Colonial Penn, AIG, and Globe Life serve an otherwise “uninsurable” population profitably.

Traditional underwritten life insurance prioritizes the lowest possible premium for healthy applicants. Guaranteed life insurance flips that priority: it optimizes for access and simplicity first, accepting a higher cost per dollar of coverage as the price of certainty.

Who Is Guaranteed Life Insurance For?

Guaranteed life insurance for seniors is the product’s core use case, but it also serves a narrower band of younger applicants who have been declined elsewhere. As a rule of thumb, this product makes sense when traditional or even simplified issue coverage isn’t an option, not as a first choice for healthy applicants.

Ideal Candidates

- Seniors, typically ages 50–80, who want dedicated final expense coverage without a medical exam.

- Individuals managing chronic illness or a high-risk medical history, such as advanced diabetes, COPD, or a history of cancer treatment.

- Applicants who have been previously declined for a traditional or simplified issue

life insurance and need a fallback option.

Common Use Cases

- Covering funeral and burial costs, which the National Funeral Directors Association estimates can run from roughly $7,000 to $12,000, depending on services chosen.

- Paying off small remaining debts, such as a credit card balance or medical bills, so they don’t pass to a spouse or estate.

- Leaving a modest legacy or “final gift” to children or grandchildren, separate from a larger estate plan.