Introduction

Many people want the certainty of lifelong coverage but hesitate because traditional whole life policies feel rigid, with fixed premiums, fixed benefits, and little room to adapt as life changes. Universal life insurance (UL) was built to solve exactly that problem: it’s permanent coverage designed to flex with your income, your family, and your financial goals over time.

This guide breaks down how universal life insurance actually works, unpacks its unique cash-value engine, compares it honestly against whole life and term policies, and helps you figure out whether it belongs in your financial plan. By the end, you’ll understand not just what UL is, but how it behaves in the real world, including the trade-offs most sales brochures leave out.

Here’s the roadmap: we’ll define the policy, walk through the mechanics of premiums and cash value, compare the three major UL variations, stack UL up against whole life and term, and close with the risks a licensed advisor should walk you through before you sign anything.

What Is Universal Life Insurance?

Universal life insurance is a type of permanent life insurance policy that provides a death benefit for the insured’s entire life, as long as the policy stays in force. Unlike term insurance, it isn’t designed to expire; it’s built to last a lifetime, provided it’s funded correctly.

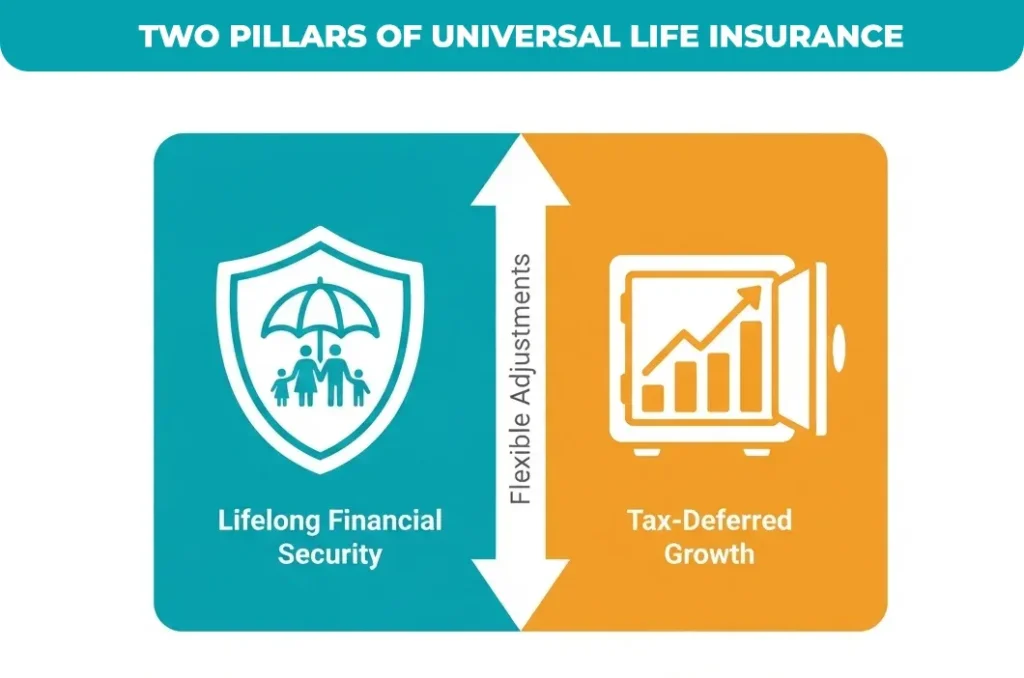

So what is a universal life insurance policy actually made of? Every UL contract rests on two pillars:

- Protect the death benefit paid to your beneficiaries, which can often be increased or decreased over the life of the policy.

- Cash Value a savings component inside the policy that accumulates over time and grows on a tax-deferred basis.

The defining feature and the reason UL exists as its own category separate from whole life is flexibility. Policyholders can generally adjust their premium payments and, within limits, their death benefit as income rises, falls, or as life circumstances change.

Expert Tip: The word ‘flexible’ in universal life insurance is a double-edged sword. I’ve seen clients pay the bare minimum premium during lean years, forget to revisit it once income improved, and not realize until their policy review that the cash value had been quietly eroding for a decade.

How Universal Life Insurance Works

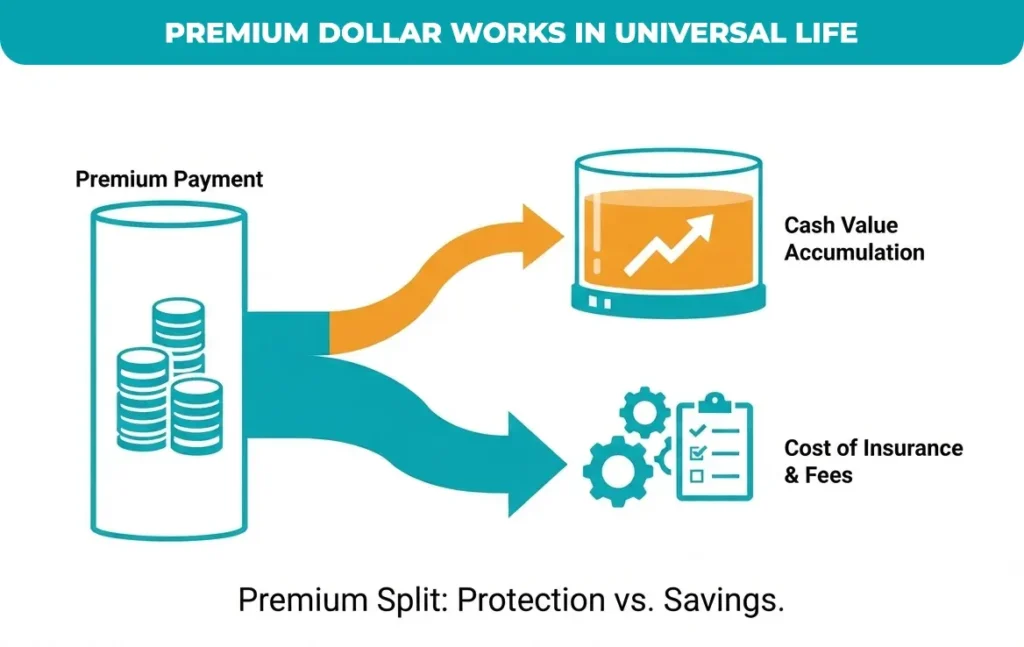

The Premium Mechanism

Each premium payment you make is split. A portion covers the cost of insurance (mortality charges) and administrative fees; the remainder is credited to the cash value account, where it grows tax-deferred.

This is fundamentally different from term life, where 100% of the premium pays for pure protection with nothing left over. In universal life insurance, the insurer discloses (or the illustration shows) how much of each dollar goes toward fees versus savings.

Flexibility in Action

Because premiums aren’t fixed the way they are with whole life, policyholders can pay less during tight financial years as long as the existing cash value can absorb the cost of insurance or pay more to build cash value faster.

The death benefit can typically be adjusted, too. A young parent might increase coverage when a child is born, then reduce it once a mortgage is paid off, and the kids are financially independent.

Accessing the Cash Value

Once cash value has accumulated, most policies allow you to borrow against it or make partial withdrawals, generally income-tax-free up to your cost basis. Loans accrue interest, and unpaid loans reduce the death benefit, an important nuance that’s often glossed over in sales pitches.

Expert Tip: Before borrowing against cash value, ask your carrier for a ‘worst-case’ illustration showing what happens to the policy if crediting rates drop and the loan is never repaid. Two clients with identical starting cash value can end up with wildly different outcomes depending on how the loan interacts with policy fees over 15–20 years.

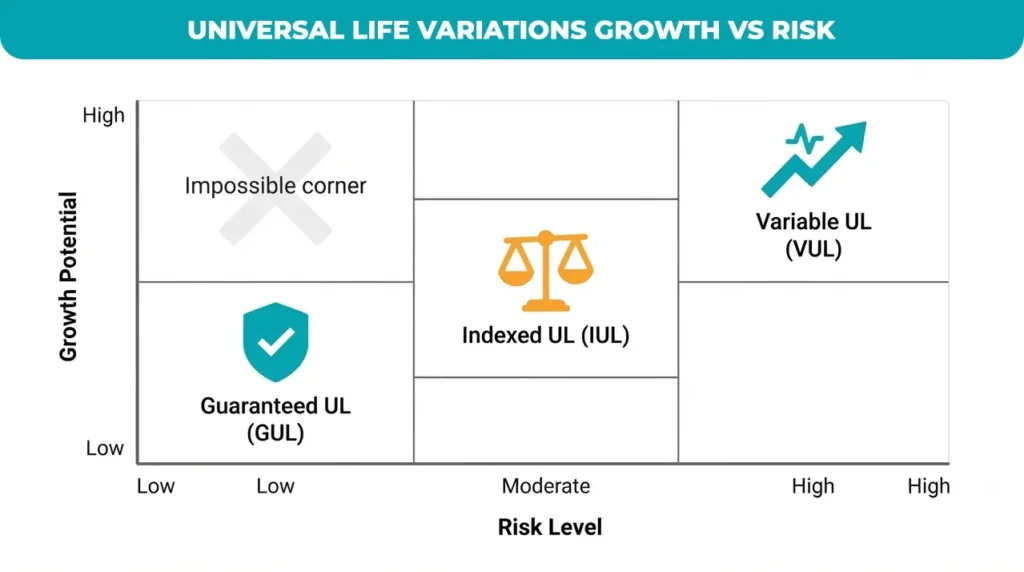

Types of Universal Life Insurance

Not all universal life insurance policies grow the same way. The three main variations differ in how the cash value earns interest and, correspondingly, how much risk the policyholder takes on.

| Type | How It Grows | Risk Level | Best For |

| Guaranteed Universal Life (GUL) | Fixed, guaranteed interest rate set by the insurer. | Low | Those who want permanent coverage with predictable costs and minimal cash-value growth expectations. |

| Indexed Universal Life (IUL) | Credited interest tied to a market index (e.g., S&P 500), with a floor (often 0%) limiting losses and a cap limiting gains. | Moderate | Those who want upside potential without direct market risk to principal. |

| Variable Universal Life (VUL) | Cash value is invested directly in sub-accounts similar to mutual funds. | High | Investors are comfortable with market volatility in exchange for higher growth potential. |

Indexed universal life insurance (IUL) has become one of the most heavily marketed variations because it promises ‘stock market gains without stock market losses.’ That’s technically true, within limits, the floor does protect principal from index losses, but caps, participation rates, and policy fees mean actual returns in an indexed universal life insurance policy are usually meaningfully lower than the index itself.

Expert Tip: When comparing indexed universal life insurance illustrations, ignore the ‘average historical return’ number insurers highlight. Ask instead for the cap rate, participation rate, and floor, as currently in force; those can change year to year and materially move your real-world return.

Universal Life vs. Other Policies: Which Is Right for You?

Universal Life vs. Term Life

Term life insurance is temporary, inexpensive, and pure protection coverage for a set period (10, 20, 30 years) with no cash value. Universal life insurance is permanent, costs more, and builds cash value alongside the death benefit. Term makes sense for a fixed obligation, like a 20-year mortgage; universal life insurance suits lifelong needs like estate planning or final expenses.

Universal Life vs. Whole Life

Whole life insurance offers fixed premiums and a guaranteed cash-value growth schedule set at issue simplicity in exchange for rigidity. Universal life insurance trades that guarantee flexibility: you can adjust premiums and benefits, but growth (outside of GUL) generally isn’t guaranteed and requires more active oversight from the policyholder.

| Feature | Term | Whole Life | Universal Life |

| Coverage Duration | Temporary (10–30 yrs) | Permanent | Permanent |

| Cash Value | None | Yes guaranteed growth | Yes, fixed, indexed, or variable growth |

| Premium Structure | Fixed, low cost | Fixed for life | Flexible, adjustable |

| Flexibility | Low | Low | High |

Key Considerations: Pros and Potential Risks

Pros

- Lifelong coverage as long as the policy remains adequately funded.

- Tax-deferred growth of cash value, with tax-free access up to basis in most cases.

- Flexibility to adjust premiums and death benefit as life circumstances change.

Risks & Responsibilities

- Policy Lapse: If premiums are underfunded and cash value can’t cover the rising cost of insurance, the policy can lapse, potentially with a tax bill on any gains.

- Active Management: Unlike whole life, universal life insurance needs periodic in-force illustrations and reviews to confirm it’s still on track.

- Non-Guaranteed Rates: Outside of guaranteed UL, interest crediting rates, caps, and participation rates can change, directly affecting how long the policy lasts.

Conclusion

Universal life insurance remains an elite, versatile strategy for those prioritizing lifelong security over rigid financial contracts. By leveraging its unique flexibility, you can masterfully adapt your protection and cash-value growth to conquer evolving life stages, ensuring your family’s legacy is shielded with precision.

Don’t settle for generic illustrations that mask potential volatility. Take command of your financial future today by scheduling a comprehensive needs analysis with a licensed professional to guarantee your policy is optimized for long-term performance and sustainable, tax-advantaged wealth building.