Introduction

Every insurance conversation eventually lands on the same fork in the road: term or whole life. The term is cheaper. Whole life costs more. On the surface, that comparison makes the decision look simple, and that’s exactly where most buyers go wrong.

A whole life insurance policy isn’t a cheaper or more expensive version of the same product. It’s a different financial instrument entirely: a permanent contract that pairs a guaranteed death benefit with fixed premiums and a tax-deferred cash value account that grows for as long as you own the policy.

This guide walks through how a whole life insurance policy actually works, how cash value accumulates, where it differs from term coverage, who tends to benefit most from owning one, and the questions worth asking before you sign an application.

What Is a Whole Life Insurance Policy?

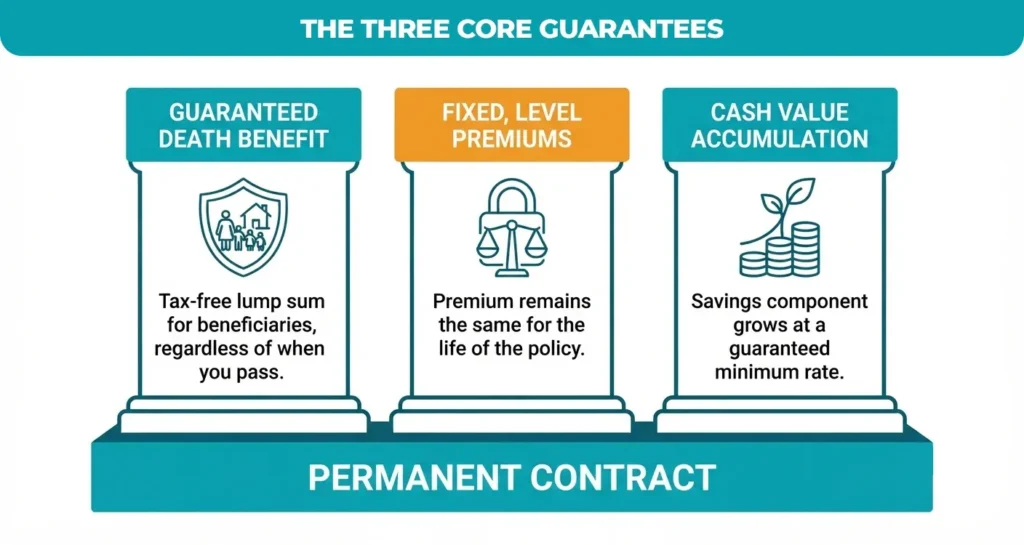

A whole life insurance policy is a type of long-term life insurance based on three fixed constants that remain constant for the duration of the contract.

The Three Core Guarantees

- Guaranteed Death Benefit: A tax-free lump sum paid to your named beneficiaries, regardless of when you pass away, as long as premiums are current.

- Fixed, Level Premiums: The premium you pay in year one is the same premium you pay in year thirty, regardless of any change in your health or age.

- Cash Value Accumulation: A savings-like component inside the policy that grows at a guaranteed minimum rate set by the insurer.

Think of a whole life insurance policy as a financial foundation rather than a single-purpose product. A term policy behaves like renting protection for a fixed period; a whole life policy behaves more like building equity in a home.

Pro-Tip: In my experience reviewing policy illustrations for clients, the biggest mistake isn’t buying whole life, it’s buying it without understanding how the insurer’s dividend scale or guaranteed column actually performs over 20 years.

How Does Cash Value Growth Work?

Tax-Deferred Compounding

A portion of every premium payment is allocated to the policy’s cash value account. That balance grows on a tax-deferred basis, meaning you owe no income tax on the growth as long as the funds remain inside the policy. Over a 20- to 30-year holding period, that deferral compounds meaningfully compared to a fully taxable account earning the same nominal rate.

Accessing Funds

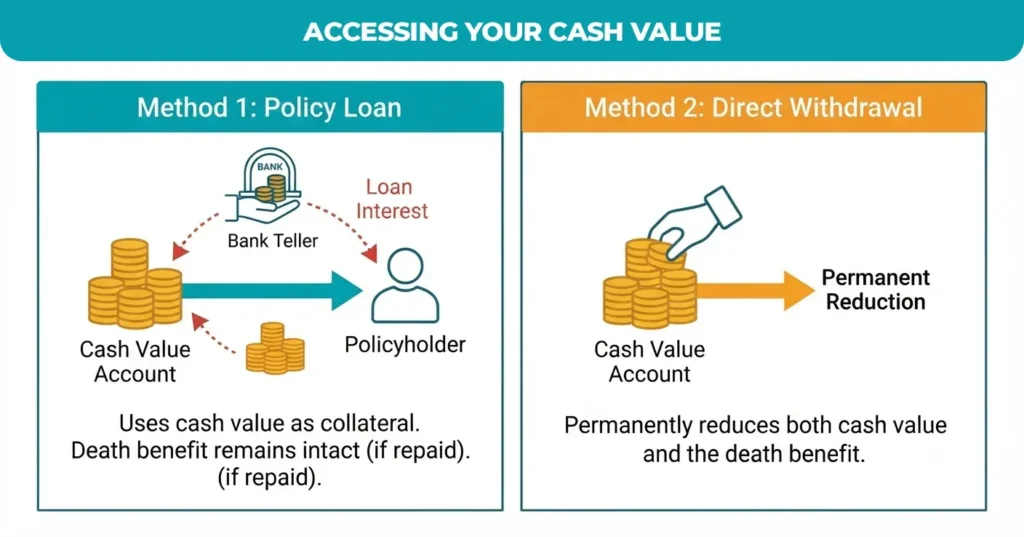

Policyholders typically access cash value in one of two ways: a policy loan, which uses the cash value as collateral and accrues interest while leaving the death benefit largely intact if repaid, or a direct withdrawal, which permanently reduces both the cash value and the death benefit. Unpaid loan balances plus interest are deducted from the death benefit if the insured passes away before repayment.

Dividends and Paid-Up Additions

Whole life policies issued by mutual insurance companies may pay annual dividends, which are technically a return of excess premium rather than guaranteed income. Policyholders can take dividends as cash, apply them toward premiums, or reinvest them as Paid-Up Additions, small increments of fully paid-up insurance that increase the death benefit.

Pro-Tip: Reinvesting dividends as Paid-Up Additions is one of the most underused levers in a whole life insurance policy. Assurance Gurus regularly runs side-by-side illustrations for clients showing dividends taken in cash versus reinvested as PUAs. The compounding difference over 25 years is often the single biggest driver of total policy value.

Whole Life Insurance vs. Term Life Insurance: Key Differences

The comparison below reflects the structural differences buyers most often ask about when weighing a whole life insurance policy against term coverage.

| Feature | Whole Life Insurance | Term Life Insurance |

| Coverage Duration | Lifetime, as long as premiums are paid | Specified term (10, 20, or 30 years) |

| Premiums | Level and guaranteed never to increase | level throughout the term, then rapidly rises upon renewal |

| Cash Value | Yes, grows on a tax-deferred basis | No cash value component |

| Cost (same face amount) | Typically 6–10x higher premium | Lower initial premium |

| Underwriting at Expiration | Not applicable coverage is permanent | Renewal or conversion may require new underwriting |

Strategic Use Case

A practical rule of thumb: use term life insurance for temporary, quantifiable obligations, such as a 30-year mortgage, income replacement until children are financially independent, or business loan collateral with a fixed payoff date. Reach for a whole life insurance policy when the need is permanent estate liquidity, final expenses, a legacy gift, or supplemental tax-advantaged savings that you want protected from market volatility.

Who Should Consider a Whole Life Insurance Policy?

Target Audience Profiles

- High-income earners who have maximized tax-advantaged retirement accounts and want another vehicle for tax-deferred growth.

- Families concentrated on generational wealth transfer, in which an inheritance is funded by a guaranteed death benefit independent of market conditions.

- Business owners who use policy cash value for liquidity, key-person coverage, or funding a buy-sell agreement between partners.

The Role of Riders

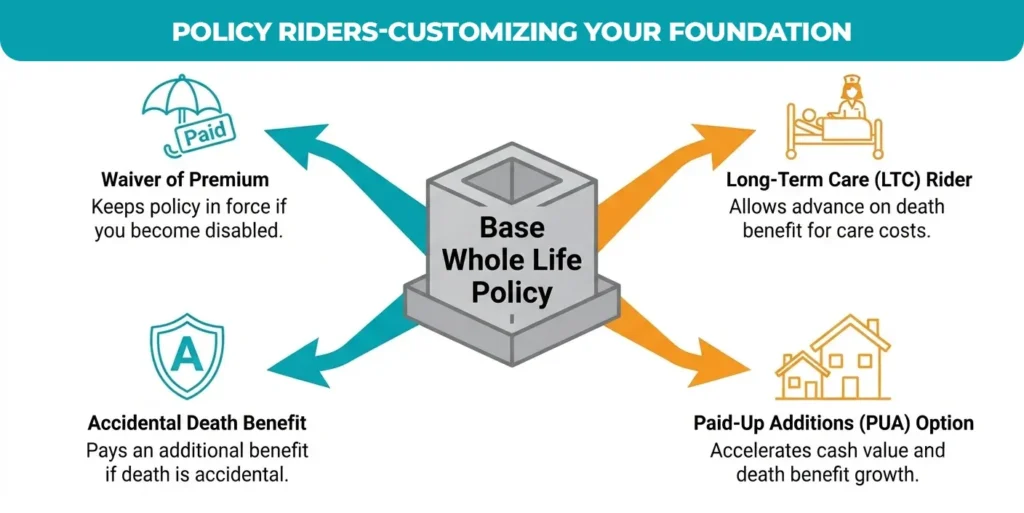

Most carriers allow policyholders to customize a base whole life insurance policy with riders such as a Waiver of Premium (which keeps the policy in force if you become disabled), Long-Term Care or Chronic Illness riders (which allow an advance on the death benefit for qualifying care costs), and Accidental Death riders (which pay an additional benefit if death results from an accident).

Pro-Tip: When business owners come to us asking about buy-sell funding, the rider selection often matters more than the base policy design. Open Care Life Insurance typically models at least two rider configurations against the client’s actual balance sheet before recommending a structure.

Common Myths and Misconceptions

It’s Only for the Wealthy

Whole life insurance policies are frequently marketed to high-net-worth households, but the underlying tool, permanent, guaranteed coverage paired with forced savings, is equally relevant to middle-income families who want predictability more than they want to chase returns.

The Cash Value Is a High-Yield Investment

A whole life insurance policy is not designed to compete with equities on rate of return, and evaluating it that way sets the wrong expectation from day one. Its value proposition is safety, tax deferral, and guarantees a bond-like allocation with a death benefit attached, not a substitute for a diversified investment portfolio.

You Can’t Touch the Money

Policy loans make cash value accessible, typically within days of a request, without credit underwriting. The trade-off is that unpaid loan interest compounds and reduces the death benefit, a real cost, but not the same as money being permanently locked away.

Steps to Choosing the Right Policy

Assess Financial Obligations

Start by calculating a death benefit need based on outstanding debt, income replacement for dependents, and future obligations such as college funding. Most planners use a multiple of income (commonly 10–15x) as a starting point, then adjust for existing assets and other coverage.

Evaluate Insurer Financial Strength

Because a whole life insurance policy is a decades-long promise, the insurer’s financial strength matters as much as the policy design. Check independent ratings from agencies such as A.M. Best or Moody’s, and review the carrier’s historical dividend payment record, not just its current dividend scale.

Conclusion

A whole life insurance policy is a long-term commitment, not a short-term product decision. What it offers in exchange for a higher premium is predictability: a death benefit that never expires, premiums that never increase, and a cash value account that compounds on a tax-deferred basis regardless of what happens in the broader market. Whether that trade-off makes sense for your financial plan depends entirely on your specific obligations.

Not sure if a whole life insurance policy is the right fit for your unique financial journey? Contact our licensed advisors at Open Care Life Insurance and Assurance Gurus for a personalized, no-obligation policy review today. We are ready to help you navigate your options and secure the legacy you have worked so hard to build.