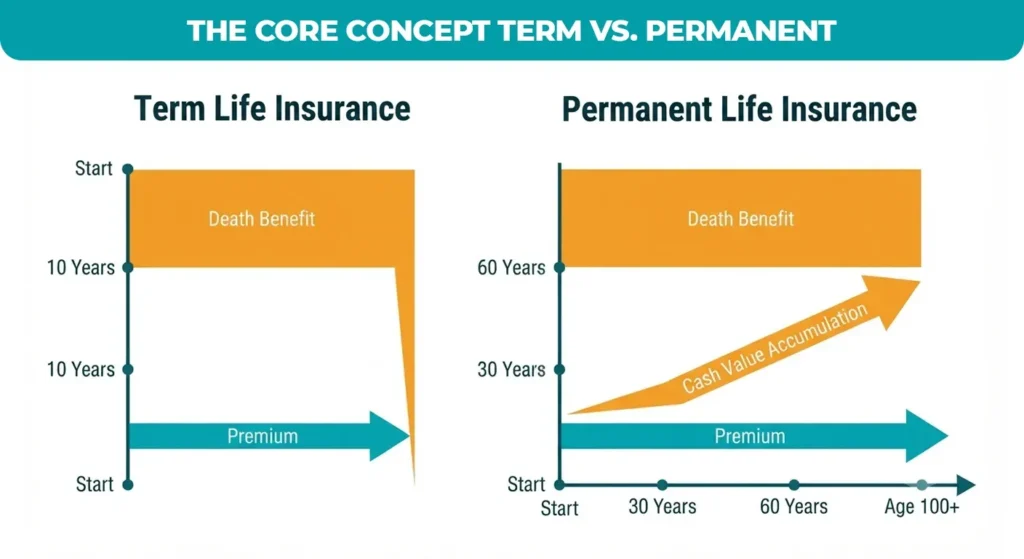

Term life insurance is built to disappear. You pick a 10, 20, or 30-year window, pay a relatively low premium, and if you outlive the term, the coverage simply ends. Permanent life insurance works differently: as long as premiums are paid, the policy never expires, and a portion of every payment builds a cash value you can access while you’re still alive.

That distinction, temporary protection versus a lifelong, growing asset, is why permanent life insurance is often discussed less as a “just in case” purchase and more as a financial planning tool. A pattern that shows up constantly when reviewing client policies: people who bought permanent coverage purely for the death benefit are often surprised, years later, by how much the cash value has grown and how little of that growth matched the illustration they were originally shown.

This guide breaks down how a permanent life insurance policy actually works, the main types of permanent life insurance available, what the cash value component really does, and a candid look at who should and shouldn’t buy one.

What Is Permanent Life Insurance?

Permanent life insurance is a life insurance category designed to provide coverage for your entire life, rather than for a fixed number of years, as long as scheduled premiums are paid. Unlike what a quick term vs permanent life insurance search might suggest, “permanent” isn’t a single product; it’s an umbrella term covering several policy structures, each with different rules for premiums, death benefits, and cash value growth.

The feature that separates every permanent life insurance policy from term coverage is the cash value account. Part of each premium payment is allocated to this account, where it accumulates on a tax-deferred basis similar in spirit to a retirement account, though it isn’t one and doesn’t carry the same contribution rules.

| Feature | Term Life Insurance | Permanent Life Insurance |

| Coverage Length | Fixed period (10-30 years) | Entire lifetime |

| Premiums | Lower, fixed for the term | Higher, fixed, or flexible by type |

| Cash Value | None | Grows tax-deferred |

| Renewability | Expires or renews at a higher rate | Continues for life if premiums are paid |

| Best For | Temporary needs: mortgage, income replacement | Lifelong needs, estate planning, and cash accumulation |

What Are the Types of Permanent Life Insurance?

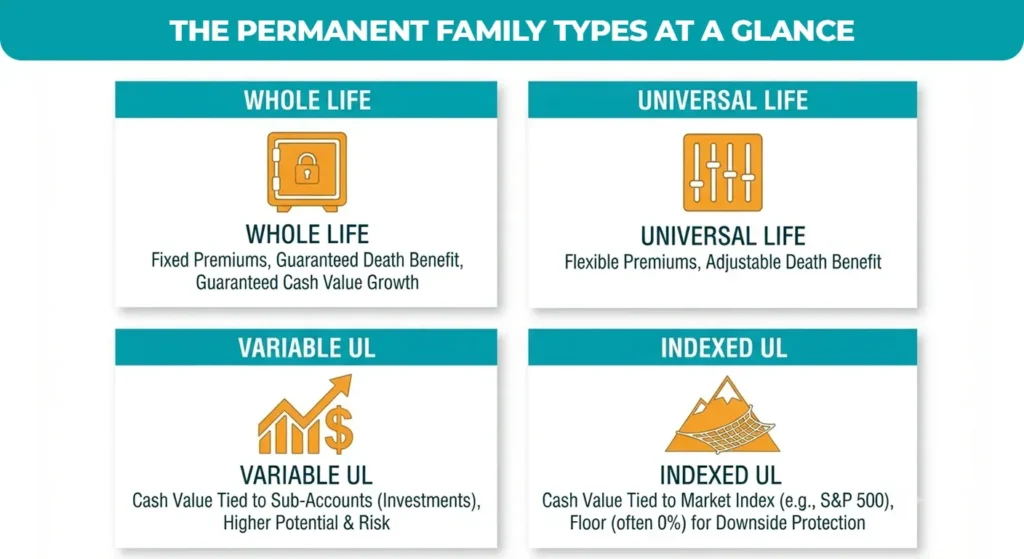

Not all permanent whole life insurance and permanent life insurance policies work the same way. Four structures dominate the market.

Whole Life Insurance

Whole life insurance is the most rigid and often the most predictable type of permanent policy. Premiums are fixed for the life of the policy, the death benefit is guaranteed, and the insurer guarantees a minimum rate of cash value growth. Policies from mutual insurance companies may also pay annual dividends, which policyholders can take as cash, use to reduce premiums, or reinvest to buy additional coverage.

Universal Life Insurance

Universal life insurance trades some of that rigidity for flexibility. Policyholders can adjust premium payments and, within limits, the death benefit itself, as cash value and interest rates fluctuate. That flexibility is attractive, but an underfunded universal life policy can lapse if cash value drops too low to cover the ongoing cost of insurance.

Variable Universal Life (VUL)

Variable universal life insurance ties cash value growth to sub-accounts that function similarly to mutual funds. This gives policyholders more control and higher growth potential, but also real downside risk; a poor market stretch can shrink cash value and even threaten the death benefit if premiums aren’t adjusted.

Indexed Universal Life (IUL)

Indexed universal life insurance has a floor (often 0%) that guards against market fluctuations while tying cash value growth to the success of a market index, like the S&P 500. losses and a cap that limits how much upside is actually captured. Industry sales data tracked by LIMRA has repeatedly shown indexed universal life as one of the fastest-growing segments of the permanent life insurance market, largely because of that downside protection.

How Does the Cash Value Component Work?

Cash value life insurance grows a policyholder’s cash value account through a mix of guaranteed interest, dividends, or index-linked or investment-linked returns, depending on the policy type. Because growth is tax-deferred, gains generally aren’t taxed each year the way they might be in a standard brokerage account.

There are two primary ways to access that money while you’re alive:

- Policy Loans: You borrow against the cash value, typically at a stated interest rate, without triggering income tax on the amount borrowed.

- Withdrawals: You take a portion of the cash value directly. Withdrawals up to your cost basis (total premiums paid) are usually tax-free; amounts beyond that may be taxable.

What Are the Key Benefits of Permanent Life Insurance?

- Lifelong Coverage: Beneficiaries stay protected no matter how old you are when you pass away, as long as premiums are current.

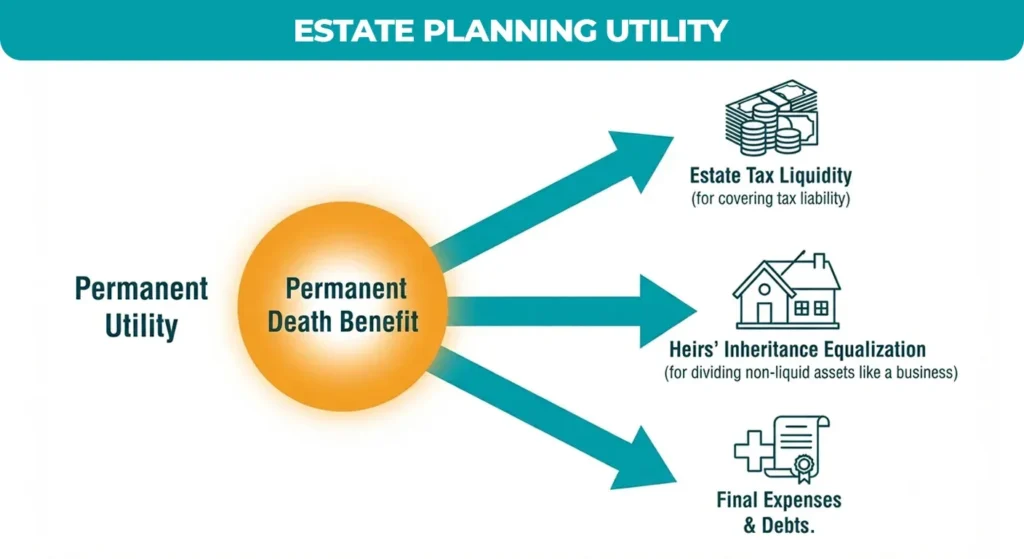

- Estate Planning Utility: The death benefit can provide immediate liquidity for heirs, covering estate taxes, final expenses, or an equal inheritance for a family business that would otherwise be divided.

- Financial Diversification: Certain permanent policies, especially whole life, act as a “sleep well at night” asset whose cash value isn’t directly tied to stock market swings.

- Potential for Dividends: Mutual insurance companies, owned by policyholders rather than shareholders, may pay annual dividends not guaranteed, but with a long track record at several major carriers.

Is Permanent Life Insurance Right for You? Term vs. Permanent

The honest answer: permanent life insurance is not the right fit for most people, and it’s worth saying so plainly. It tends to make the most sense for:

- High-net-worth individuals focused on estate tax liquidity

- Parents or guardians of dependents with lifelong needs, such as special needs children

- Business owners funding buy-sell agreements or key-person coverage

- Savers who have already maxed out 401(k)s, IRAs, and other tax-advantaged accounts and want another tax-deferred bucket

The “Buy Term and Invest the Difference” Argument: This is the core of the Dave Ramsey permanent life insurance critique. Ramsey and other consumer-finance advocates argue that affordable permanent life insurance is rarely worth it; instead, buy inexpensive term coverage and invest the premium difference in low-cost index funds, which have historically outperformed a policy’s internal cash value growth rate. It’s a reasonable argument for someone who will actually invest the difference consistently. In practice, the people who benefit most from permanent life insurance are those who’ve demonstrated they won’t do that or who need the estate planning and liquidity features that term insurance simply doesn’t provide.

Common Misconceptions About Permanent Life Insurance

- Permanent life insurance is the same as whole life insurance. Whole life is one type of permanent policy; universal, variable universal, and indexed universal life are also permanent, but work differently.

- The cash value is extra money on top of the death benefit. In most policies, the amount paid to beneficiaries is the face amount, not the face amount plus remaining cash value.

- Permanent life insurance is always a bad investment. It isn’t designed to be judged purely on investment returns; its value includes guaranteed lifelong coverage and tax treatment a brokerage account doesn’t offer.

- Once you buy it, the premium can’t change. True for whole life, but universal and variable universal life premiums and death benefits can flex, and an underfunded policy can lapse.

Conclusion

Ultimately, permanent life insurance represents a significant, long-term financial commitment that requires careful deliberation rather than a hasty decision based on a single conversation. When viewed through the correct lens, it functions less like a standard “death benefit product” and more like a robust, sophisticated financial planning tool. This adaptable asset can support tax-advantaged growth, guarantee steadfast protection, and effectively complement your overall estate strategy.

Before you finalize any purchase, take the proactive step of requesting a personalized illustration from a trusted, licensed agent or fiduciary advisor to clearly see the guaranteed and non-guaranteed values specific to your age, health class, and desired coverage amount. Relying on the generic numbers found in a standard brochure is rarely sufficient, as they seldom reflect the reality of your unique financial journey.