Introduction

Life insurance has a reputation as a young family’s product, something you buy in your thirties to protect a mortgage and small children. That reputation is outdated. For seniors, the best life insurance for seniors is a legacy-planning tool: it covers final expenses, pays off lingering debt, and hands the next generation a tax-free inheritance instead of a stack of bills.

Many older adults assume that once they pass a certain age, or once a diagnosis appears on their chart, they become “uninsurable.” Others assume any policy that will accept them must be unaffordable. Neither assumption holds up. Insurers have built entire product lines from simplified-issue term policies to guaranteed-acceptance whole life specifically for applicants in their 60s, 70s, and 80s.

This guide demystifies the options available in 2026, from Whole Life to Guaranteed Issue, and walks through the practical, step-by-step process for finding coverage that fits your health profile and your budget.

Why Do Seniors Need Life Insurance Beyond Just Final Expenses?

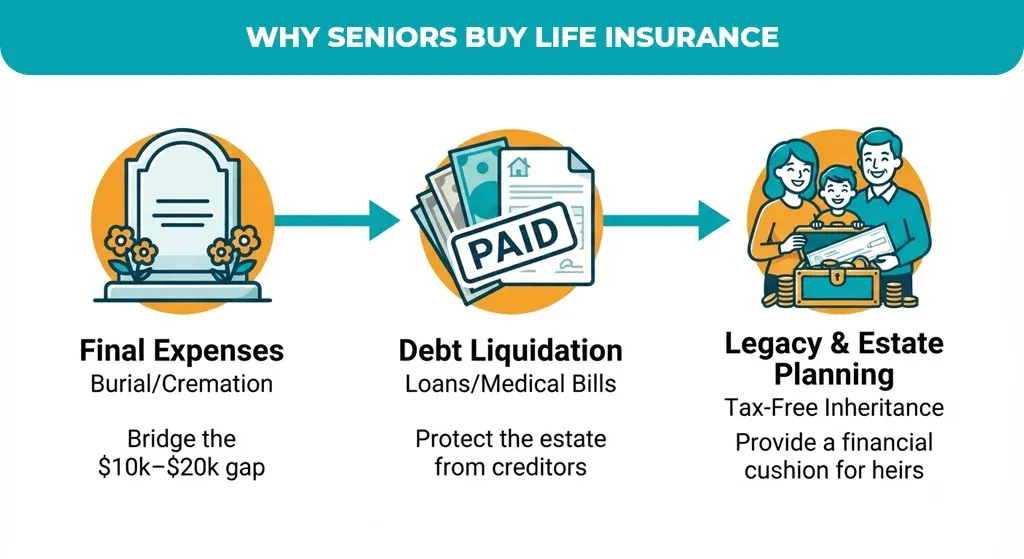

Life insurance for older adults functions as a financial bridge between what a person leaves behind and what their family is left owing. Three needs typically drive the purchase decision.

Covering Rising Final Expense and Burial Costs

Funeral costs have climbed steadily. The National Funeral Directors Association (NFDA) puts the median cost of a funeral with viewing and burial at roughly $8,300, and a funeral with cremation at about $6,280 figures climb to $11,000–$13,000 once a cemetery plot, vault, headstone, and reception are added. Source: National Funeral Directors Association. A dedicated final expense or burial insurance policy, typically in the $10,000–$20,000 range, is sized to close that exact gap.

Liquidating Debt So It Doesn’t Pass to Heirs

Mortgages, medical bills, and personal loans don’t disappear at death; they become claims against the estate. A death benefit gives a surviving spouse or adult children the cash to settle those balances immediately, rather than liquidating investments or selling a family home under time pressure.

Legacy and Estate Planning

For higher-net-worth seniors, permanent life insurance provides liquidity to cover estate taxes without forcing the sale of property or a business. For everyone else, it is simply a clean, tax-free inheritance for beneficiaries; proceeds from a death benefit generally pass to heirs without income tax. This matters more than most people realize: research from LIMRA indicates that roughly 100 million Americans lack adequate coverage, with about 40% of adults carrying less life insurance than they actually need. Source: LIMRA U.S. Life Insurance Need Gap study.

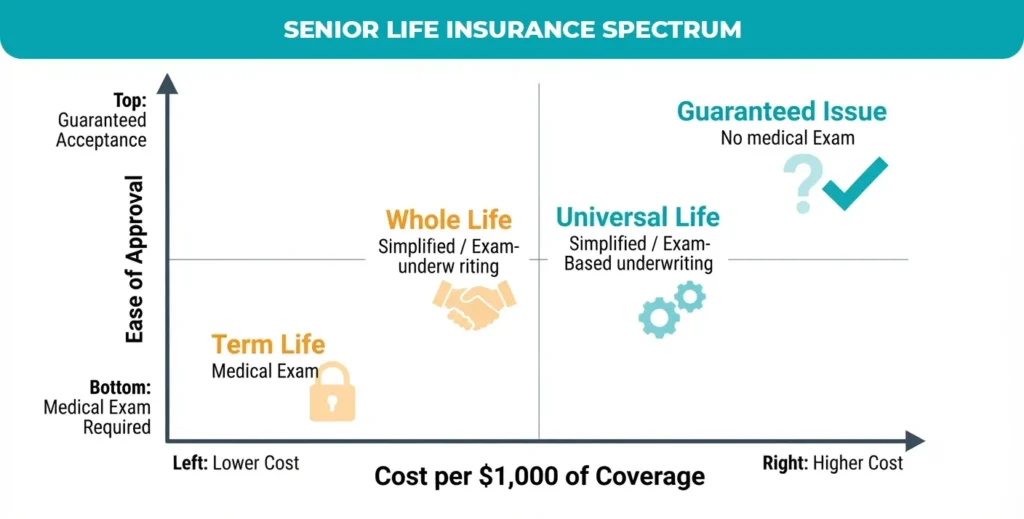

What Are the Top Types of Life Insurance for Seniors?

Choosing among the best life insurance policies for seniors starts with understanding how each product structures its premium, its underwriting, and its death benefit.

What Is the Best Whole Life Insurance for Seniors?

Whole life insurance is permanent coverage: as long as premiums are paid, the policy never expires. Premiums are level for life, and a portion of every payment builds tax-deferred cash value that a policyholder can borrow against later. This makes Whole Life the best whole life insurance for seniors who want certainty, a locked-in rate, a guaranteed payout, and a living asset they can tap if needed.

Is Term Life Insurance a Good Value for Seniors?

Term life insurance covers a fixed window of 10, 15, or 20 years and carries no cash value, which is why it is the lowest-cost option per dollar of coverage. It suits seniors who have a specific, dated obligation: finishing off a mortgage, bridging to when a pension or Social Security fully replaces income, or covering a spouse until other assets mature.

What Is Guaranteed Issue Life Insurance and Who Needs It?

Guaranteed issue life insurance is the “no-health-questions” option: applicants between roughly 50 and 85 are accepted regardless of medical history, with no exam and no health questionnaire. This makes it the best life insurance for seniors over 80 or for anyone with a serious pre-existing condition who cannot pass underwriting elsewhere.

How Does Universal Life Insurance Work for Older Adults?

Universal life insurance is permanent coverage with built-in flexibility: within limits, policyholders can adjust their premium payments and, in some cases, the death benefit itself as circumstances change. Cash value growth is tied to a fixed or indexed interest rate rather than the level guarantee found in whole life.

What Factors Influence Life Insurance Premiums for Seniors?

Insurers price every senior application around a handful of core risk factors.

- Age and health: these are the two primary drivers of cost. Every year of age and every chronic condition (diabetes, heart disease, COPD) nudges the premium upward, which is why locking in a policy sooner rather than later is almost always cheaper.

- Smoking and nicotine use: smokers routinely pay two to three times more than non-smokers for identical coverage. A 40-year-old non-smoker might pay around $29/month for a $500,000, 20-year term policy versus roughly $95/month for a smoker with the same coverage [Source: industry rate averages, 2026].

- Medical underwriting vs. no-exam: A fully underwritten policy with a paramedical exam is the cheapest per dollar of coverage because the insurer has the most information to price risk accurately. No-exam and simplified-issue policies are faster and easier to obtain but cost more per $1,000 of coverage since the insurer is taking on more uncertainty.

Comparison Table: Best Life Insurance Policies for Seniors

| Policy Type | Health Questions? | Best For | Key Trade-Off |

| Whole Life | Yes (or simplified) | Seniors wanting lifelong, level-premium coverage plus cash value | Highest premium per dollar of coverage |

| Term Life | Usually yes | A fixed-length need, like finishing a mortgage payoff | Coverage ends; renewing later costs far more |

| Guaranteed Issue | None | Seniors 70–85 with health conditions that block other coverage | 2-year graded benefit; low coverage per dollar |

| Universal Life | Yes (or simplified) | Seniors who want flexible premiums as income changes | Can lapse if underfunded; requires monitoring |

What Red Flags Should Seniors Watch for When Shopping?

The senior insurance market attracts aggressive marketing. A few habits protect against the most common traps.

- High-pressure sales tactics: walk away from any agent pushing for an immediate signature without giving time to review the policy in writing.

- Hidden fees and unnecessary riders: read every add-on rider; some inflate the premium substantially without adding meaningful value for a given health profile.

- Misleading advertising: Be skeptical of ads implying “free” coverage or a flat, universal $9.95-a-month rate. This is almost always a paid policy, and the advertised price typically applies only to a single small “unit” of coverage, with the real cost to reach a meaningful death benefit running several times higher.

Common Misconceptions About Life Insurance for Seniors

A few widely repeated claims don’t hold up once the underwriting details are examined.

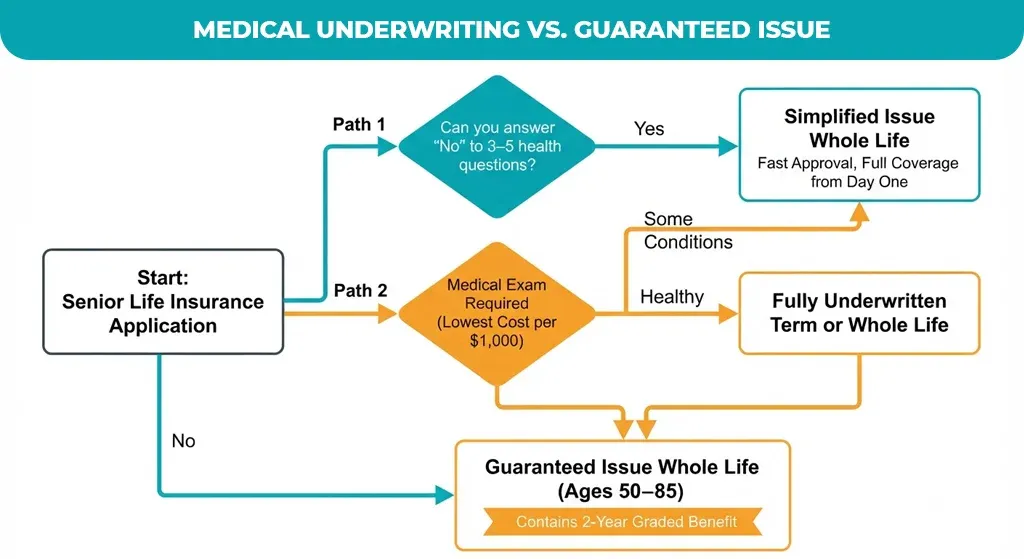

I’m too sick or too old to be eligible.

Guaranteed issue policies accept virtually every applicant between 50 and 85, regardless of health history. The real question isn’t whether coverage exists; it’s whether guaranteed issue is the cheapest path or whether a simplified-issue policy with a few health questions would provide more coverage for less money.

A cheap advertised rate means cheap coverage.

Advertised “unit” pricing (a fixed dollar amount per month) can be deceptive because the coverage each unit buys shrinks as the applicant’s age increases. A rate that looks identical across age groups can mean a 50-year-old receiving three or four times the death benefit of an 85-year-old for the same monthly cost. Always ask for the dollar amount of coverage, not just the premium.

Guaranteed issue and simplified issue are the same thing.

They are not. Simplified issue asks a short list of health questions and skips the exam; approval is fast but not universal, and coverage typically begins in full from day one. Guaranteed issue skips health questions entirely but imposes the two-year graded benefit. Most seniors who assume they need guaranteed issue actually qualify for simplified issue at a lower cost and without the waiting period.

Conclusion

Securing the best life insurance for seniors is a proactive step toward protecting your legacy and ensuring your family is not burdened by financial obligations. Whether you need a simple policy to cover final expenses or a more permanent plan to support your estate, there are viable options available for nearly every health profile and budget.

The key to finding the right protection lies in comparing multiple quotes and understanding the trade-offs between different product types. By working with a licensed, independent insurance agent, you can bypass misleading marketing and secure a policy that offers the best life insurance for seniors tailored to your specific needs, providing lasting peace of mind for you and your loved ones.

Life insurance options can feel overwhelming. You don’t have to navigate the fine print alone. The team at Premier Services Agency is here to provide the clarity you need to make an informed choice for your family.”