Introduction

That is precisely where short-term disability (STD) insurance steps in. It is a targeted safety net engineered to bridge the income gap between the day you stop working and the day you are healthy enough to return. In my 15+ years advising individuals and HR teams on insurance and financial planning, I have seen this single policy prevent more financial crises than almost any other product in a benefits package.

This guide covers everything you need to know: what short-term disability insurance is, what it covers (and what it excludes), how it differs from long-term disability coverage, how to choose the right policy, and answers to the questions I hear most often from clients.

What Is Short-Term Disability Insurance and How Does It Work?

Short-term disability insurance is a policy that replaces a portion of your income, typically 50–70% of your gross base salary, when a non-work-related illness or injury temporarily renders you unable to perform your job duties. The key word here is temporary: benefits are designed to cover a defined window of time, usually between 3 and 12 months.

Unlike health insurance (which pays your medical bills) or life insurance (which pays your beneficiaries), STD insurance pays you, directly replacing the paycheck you can no longer earn. Think of it as a parachute for your bank account.

How Does the Claims Process Actually Work?

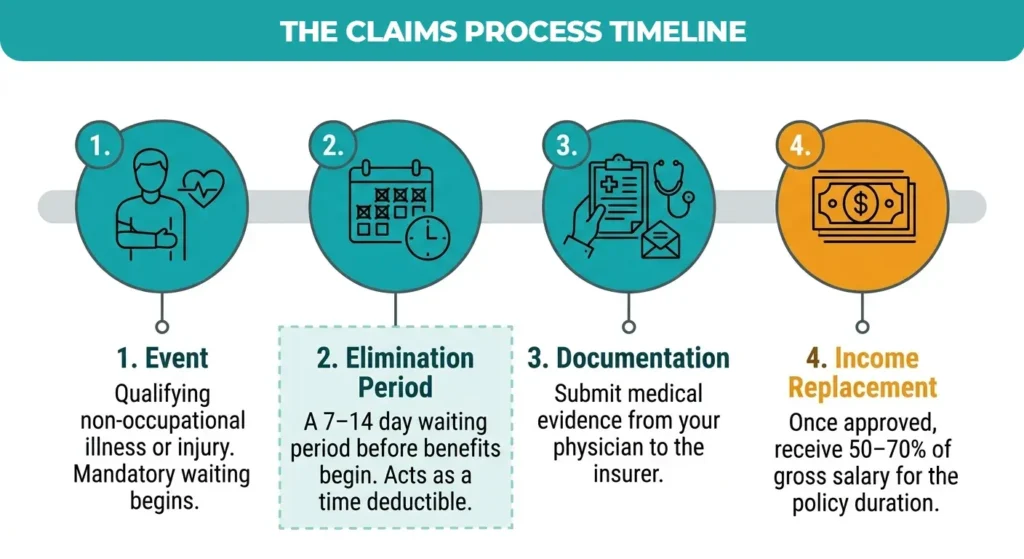

- The mechanism is straightforward. Here is the step-by-step process most private short-term disability insurance plans follow:

- An event occurs: illness, injury, or a qualifying medical condition that prevents you from performing your job duties.

- The Elimination (Waiting) Period begins. This is the mandatory waiting window, typically 7 to 14 days before benefits kick in. Think of it as the deductible measured in time rather than dollars.

- You submit a claim. This involves medical documentation from your treating physician confirming your inability to work, submitted to your insurer.

- Benefit payments begin. Once approved, you receive a percentage of your pre-disability salary, usually 50–70% on a regular basis (weekly or biweekly) for the duration of your disability or until the policy’s maximum benefit period is reached.

What Does Short Term Disability Insurance Cover? (And What It Doesn’t)

One of the most important decisions when evaluating short-term disability insurance plans is understanding the scope of coverage. The policy language matters, and unfortunately, most people never read it until they need to file a claim.

Qualifying Conditions That Are Typically Covered

- Surgical recovery, including elective procedures that result in documented inability to work.

- Accidental injuries, broken bones, soft tissue damage, head injuries from falls, car accidents, or sports.

- Serious illness, including cardiac events, cancer treatment recovery, and acute infections.

- Mental health conditions: severe anxiety disorders, clinical depression, or PTSD may qualify, depending on the specific policy language and documentation requirements.

- Pregnancy and childbirth recovery: most individual and group STD plans treat a normal pregnancy delivery as a standard disability, typically providing 6 weeks of benefits (8 weeks for a C-section). This is the most common use case I see in employer group plans.

What Short-Term Disability Insurance Does NOT Cover

- Work-related injuries or illnesses: these are covered by Workers’ Compensation, a separate state-mandated program. STD is explicitly for non-occupational disabilities.

- Pre-existing conditions: many individual short-term disability insurance policies include a look-back period (commonly 12–24 months). Conditions diagnosed or treated during that window may be excluded from coverage for a defined period.

- Self-inflicted injuries standard exclusion across virtually all policies.

- Disabilities arising from criminal activity also universally excluded.

Short Term vs. Long Term Disability Insurance: Key Differences

Both short and long-term disability insurance share the same fundamental purpose: income replacement during a disabling event, but they serve very different roles in a comprehensive financial plan. Confusing the two, or assuming one covers what the other does not, is one of the most costly mistakes I have seen clients make.

Side-by-Side Comparison

| Feature | Short-Term Disability | Long-Term Disability |

| Benefit Duration | 3–12 months | 2 years to lifetime |

| Waiting Period | 7–14 days | 90–180 days |

| Income Replacement | 50–70% of gross salary | 50–60% of gross salary |

| Coverage Trigger | Temporary illness/injury | Severe or chronic condition |

| Cost (% of salary) | 1–3% annually | 1–4% annually |

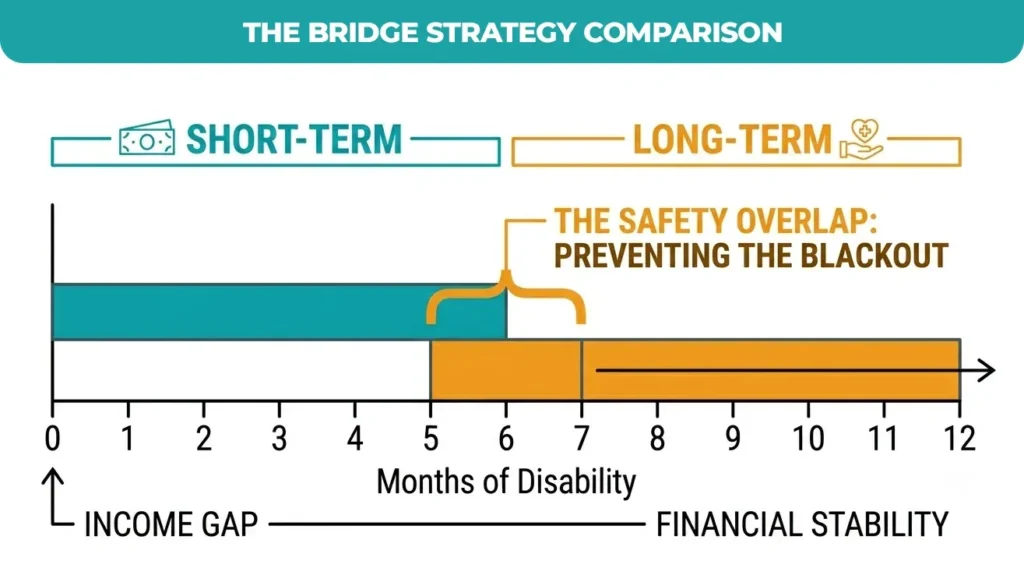

The ‘Bridge’ Strategy: Using Both Policies Together

The most effective approach and what I consistently recommend to clients who can afford it is to hold both policies simultaneously. Short-term disability handles the immediate gap: the weeks and months following an injury or illness. Long-term disability, with its 90–180 day elimination period, then activates to cover extended or permanent disabilities.

When the STD benefit period ends, and a long-term disability claim is still being evaluated or hasn’t yet kicked in, many individuals face a dangerous income blackout. Coordinating benefit periods and elimination periods between your short- and long-term disability insurance policies eliminates this gap.

| Pro TipWhen purchasing both policies, ensure the end of your STD benefit period overlaps, even by 30 days, with the activation of your long-term disability benefits. A single week of income blackout between the two can force premature return to work and worsen a medical condition. |

How to Choose the Right Short Term Disability Policy

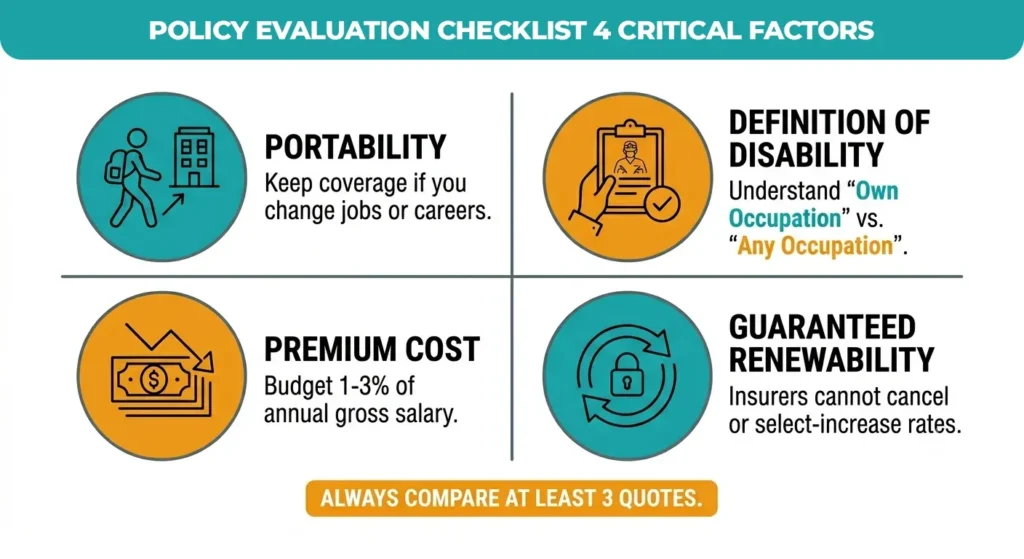

Whether you are evaluating an employer-sponsored group plan or exploring private short term disability insurance as a self-employed professional, the variables that matter most come down to four factors: cost, definitions, portability, and renewability.

Employer-Sponsored vs. Individual Short Term Disability Insurance

- Group plans (employer-sponsored): These are typically cheaper because the risk is spread across many employees. The employer often covers part of the premium. The downside: you cannot take the policy with you if you change jobs, and the coverage terms are not customizable.

- Individual short-term disability insurance: Purchased through a private broker or insurer, these plans are fully portable, meaning you keep the coverage regardless of your employment status. They are the right choice for self-employed individuals, freelancers, and anyone in a career transition.

Critical Policy Features to Evaluate

- Definition of Disability: This is the single most important clause in any STD policy. ‘Own occupation’ disability means you are considered disabled if you cannot perform the specific duties of your current job. ‘Any occupation’ means you are only considered disabled if you cannot perform any job at all.

- Premium Costs: Short-term disability insurance for individuals typically costs 1–3% of annual salary. A worker earning $60,000 per year should budget $600 to $1,800 annually for a standalone private plan.

- Policy Portability: Can you keep the policy if you leave your current employer? For individual plans, the answer is almost always yes. For group plans, it depends on whether the policy allows conversion.

- Guaranteed Renewability: A guaranteed renewable policy means the insurer cannot cancel your coverage, increase your rate selectively, or alter terms as long as you continue paying premiums. This clause is non-negotiable for a serious policy.

| Expert InsightShort-term disability insurance quotes can vary dramatically, sometimes by 40–50%, for functionally identical coverage between carriers. The variables are the insurer’s underwriting philosophy, your industry (manual labor vs. desk job), age, and health history. Always compare at least three short-term disability insurance quotes before purchasing. |

Conclusion

Short-term disability insurance may lack glamour, but it acts as a critical financial stabilizer, often determining whether families survive unexpected health crises with their finances intact. Since the average American is only one major medical event away from a significant setback, securing a well-structured short-term disability policy—whether through an employer-sponsored group plan or a private, portable individual policy—remains one of the most cost-effective strategies to protect your primary income stream.

Start your evaluation today by auditing your current employee benefits handbook to confirm your specific elimination period, income replacement ratio, and total benefit duration. If you identify an “income blackout” gap between your short-term benefits and long-term disability coverage, or if you are self-employed and lack professional safety nets.

Ready to secure your income?

At Premier Services Agency, we specialize in helping individuals and professionals find the right disability coverage that fits their unique needs and budget. Contact our expert team at Premier Services Agency.

Frequently Asked Questions

Can I purchase short-term disability insurance on my own?

Yes, private short-term disability insurance is accessible through independent brokers, financial advisors, or direct carrier websites. This is the primary option if you are self-employed or lack employer-sponsored group coverage benefits.

Does Sjögren’s syndrome qualify for disability?

It can qualify if the condition acutely worsens, preventing you from performing job duties. Success depends on thorough medical evidence demonstrating functional impairment, which helps insurers approve claims for severe, documented autoimmune flares.

How exactly does short-term disability work?

It replaces 50–70% of your gross salary during a temporary illness or injury. Benefits begin after a mandatory elimination period, usually 7 to 14 days, and continue until you recover or the maximum duration.

Does having multiple sclerosis qualify for disability?

An acute relapse preventing work may qualify for benefits. However, policies often exclude MS as a pre-existing condition if diagnosed previously, so carefully review your exclusion riders and disclose your full health history.