Introduction

Think of a life insurance plan not as paperwork you sign because you have to, but as the most deliberate financial decision you will ever make for the people you love most. It is a written promise that your family’s mortgage gets paid, your children get their college education, and your spouse does not have to abandon their lifestyle, regardless of what life delivers.

Yet millions of households remain dangerously exposed. Studies consistently show a massive protection gap, with many families either carrying zero coverage or policies so small they would not cover a single year of lost income.

This guide changes that. You will learn exactly what each life insurance plan type does, how to calculate the precise coverage amount your family needs, what drives your premium up or down, and how to pick a provider you can actually trust to pay a claim decades from now.

What Are Life Insurance Plans and Why Do They Matter?

The Core Contract

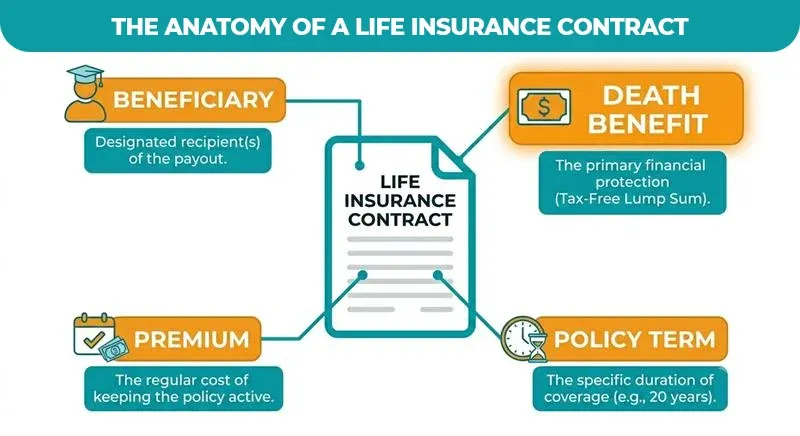

A life insurance plan is a legally binding contract between you (the policyholder) and an insurance company. You pay regular premiums monthly, quarterly, or annually. In return, the insurer guarantees a lump-sum payment called the death benefit to your chosen beneficiary when you die.

That single sentence contains three terms worth knowing cold:

- Death Benefit: The tax-free lump sum paid to your family. A $500,000 death benefit means your family receives $500,000, not $500,000 minus income tax.

- Beneficiary: The person or entity you designate to receive the death benefit. You can name multiple beneficiaries and specify percentage splits.

- Premium: Your cost of keeping the policy active. Miss enough payments and most policies lapse, leaving your family unprotected.

The Main Types of Life Insurance Plans

Term Life Insurance: Pure, Affordable Protection

Term life insurance is the financial world’s purest protection product. You choose a coverage period, typically 10, 15, 20, or 30 years, and pay a fixed premium throughout. If you die within that term, the death benefit is paid. The policy expires with no payout if you live longer than the period.

This simplicity is its greatest strength. A healthy 35-year-old can often secure a $500,000, 20-year term life insurance plan for less than the price of a daily coffee. It is the go-to choice for families with a mortgage, young children, or a working spouse who depends on their income.

Affordable life insurance plans almost always start here. Term is where cost-conscious families get the most protection per dollar.

Permanent Life Insurance: Coverage That Never Expires

Permanent life insurance stays in force for your entire life, provided premiums are paid. The two dominant forms are:

- Whole Life Insurance Plans: Fixed premiums, a guaranteed death benefit, and a cash value component that grows at a set rate. Predictable, stable, but more expensive than term.

- Universal Life Insurance Plans: Flexible premiums and death benefit amounts, with cash value tied to market interest rates. The ” grow-up ” plan life insurance concept, building cash value you can borrow against, typically refers to permanent policies like these.

How Much Coverage Do You Need? The DIME Formula

The most dangerous number in life insurance is a guess. Agents who tell you ‘ten times your income’ are using a shortcut that often leaves families underinsured. The DIME formula used by certified financial planners calculates your actual needs from four measurable inputs.

| Letter | Component | What to Calculate | Example |

| D | Debt | All non-mortgage debt (credit cards, auto loans, personal loans) | $45,000 |

| I | Income | Annual salary x years of replacement needed (typically 10–15 years) | $60,000 x 12 = $720,000 |

| M | Mortgage | Current outstanding mortgage balance | $285,000 |

| E | Education | Estimated 4-year college cost per child (inflation-adjusted) | $120,000 per child |

Running the DIME Calculation

Add all four components together. Using the examples above:

- D (Debt): $45,000

- I (Income): $720,000

- M (Mortgage): $285,000

- E (Education): $240,000 (two children)

Total DIME Coverage Needed: $1,290,000

PRO TIP: The Inflation Buffer: Add 15–20% to your DIME total to account for inflation. A policy structured in 2026 must still deliver real purchasing power in 2041. Education costs alone have historically grown at 5–6% annually.

Factors That Influence Your Premium

Insurance underwriting is risk science. Every factor below is a data point that actuaries use to predict your life expectancy and price your policy accordingly.

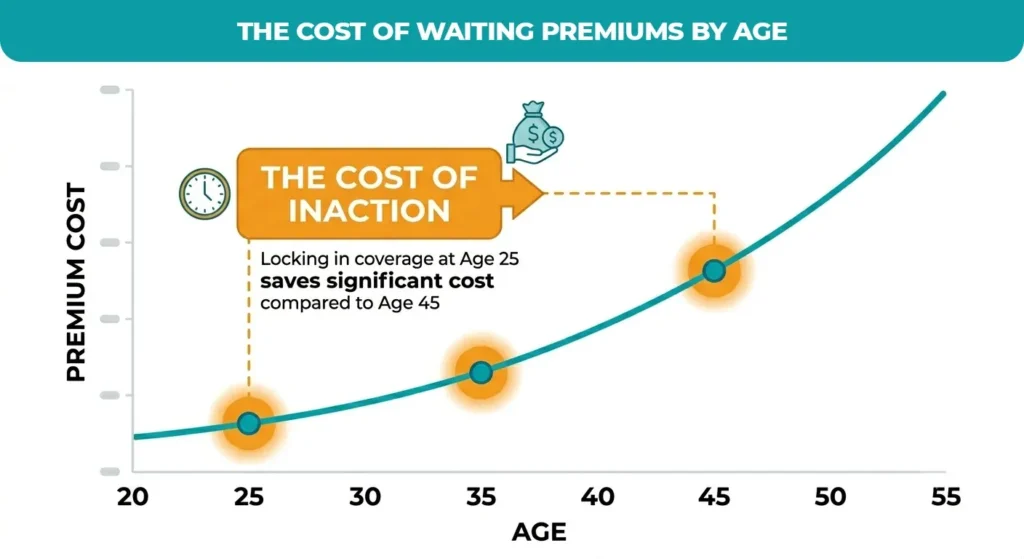

Age and Health: Lock In Rates Early

A 30-year-old buying the same policy as a 45-year-old will pay dramatically less, often 40–60% less for identical coverage. Your health status at the time of application is frozen into your premium. A rating for high blood pressure at 45 cannot be retroactively removed even if you improve your health later.

Security plan life insurance strategies often recommend buying early, locking in low rates, and laddering multiple smaller policies with different expiry dates rather than buying one large policy at middle age.

Lifestyle Choices: The Smoking Penalty

Smokers typically pay two to three times the premium of non-smokers for identical coverage. Most insurers apply the smoker rate for any tobacco or nicotine use in the past 12 months, including vaping. Quitting and maintaining a 12-month clean record before applying can save tens of thousands of dollars over a policy’s life.

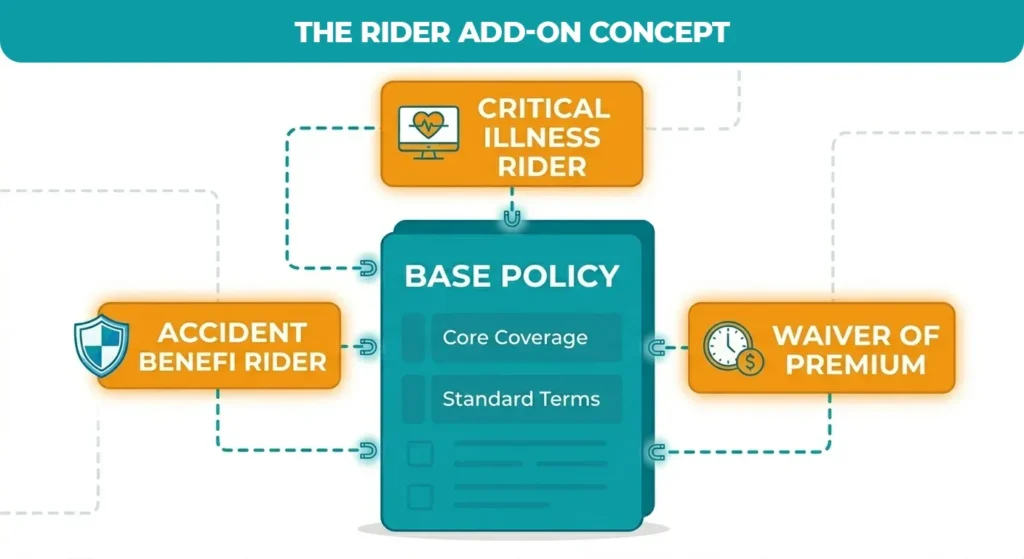

Customizing Your Plan: Riders and Flexibility

A rider is an optional provision that modifies your base policy, adding, restricting, or conditioning benefits. Think of riders as add-ons to a base model car: the car works without them, but the right additions make it significantly more useful.

Critical Illness Rider

Pays a lump sum upon diagnosis of a covered condition, typically a heart attack, stroke, or cancer, regardless of whether you die. This protects against the financial devastation of surviving a serious illness: lost income, medical bills, and recovery costs. Family life insurance plans that include a critical illness rider address both living benefits and death benefits in one policy.

Waiver of Premium

If you become totally disabled and cannot work, the waiver of premium rider keeps your policy in force without requiring premium payments. This ensures your family is not left unprotected precisely when your earning power has already been eliminated.

Conclusion

Securing a term life insurance plan is the most decisive, high-impact step you can take to architect your family’s absolute financial independence. By prioritizing this essential safety net today, you replace paralyzing uncertainty with ironclad security, ensuring your loved ones are shielded from catastrophe regardless of life’s unpredictable turns.

Do not wait for a life-changing event to evaluate your coverage; the optimal time to lock in rock-bottom premiums is while you are young and healthy. Take control of your legacy now, compare personalized quotes from top-rated providers, and invest in the incomparable peace of mind that comes from knowing your future is protected, guaranteed, and fully secure.

Ready to Protect Your Family’s Future?

Take the first step toward absolute financial independence today. At Premier Services Agency, we help you navigate the complexities of life insurance by aligning your coverage with your specific DIME needs.

Frequently Asked Questions

Which four categories of life insurance exist?

The four primary types are term life, which offers fixed-period protection; whole life, providing permanent coverage with guaranteed cash value; universal life, offering flexible premiums; and variable life, featuring investment-linked cash value.

What is the monthly cost of a $100,000 life insurance policy?

Costs vary by age, but a healthy 25-year-old pays $8–$12 monthly, while a 55-year-old pays $50–$80. These figures are illustrative; your exact premium depends on health history, chosen insurer, and specific policy terms.

Can someone with a pacemaker get life insurance?

Yes, a pacemaker does not automatically disqualify you. Underwriters evaluate the underlying cardiac condition and your current heart function. Working with an independent broker helps you find insurers experienced with cardiac-related medical cases.

Can a person with dementia get life insurance?

Early-stage cognitive impairment may qualify for coverage with some carriers at higher rates. Moderate-to-severe cases generally preclude approval, though alternatives like guaranteed issue or final expense policies might be available for older applicants.

Is the Death Benefit Taxable?

In the United States, death benefits paid directly to an individual beneficiary are generally not subject to federal income tax. However, if the death benefit is paid to an estate, it may be subject to estate taxes depending on the total estate value. Interest earned on death benefits held by the insurer before disbursement is taxable.