Introduction

When a loved one passes, the last thing any family should be thinking about is money. Yet the average American funeral now costs between $7,848 and $12,000, a figure that climbs higher when you add burial insurance, headstones, and reception costs. Most families receive no warning. They have 72 hours to make decisions worth thousands of dollars while in the depths of grief.

A Funeral Advantage plan, also called final expense insurance or burial insurance, solves this problem proactively. It removes the financial burden from surviving family members and allows them to focus on honouring a life, not managing a financial crisis.

In our experience working with seniors and estate planners, the families who struggle most are not those without money; they are the ones who never had a clear plan. This guide covers everything you need to know to make an informed decision about Funeral Advantage insurance, from how it works to how to pick the right policy.

What Is a Funeral Advantage Plan?

A Funeral Advantage plan is a small whole-life insurance policy with one specific purpose: paying for end-of-life expenses. Unlike a traditional life insurance policy designed for income replacement, this product is engineered for immediate, targeted liquidity funds your beneficiary can use within days to pay a funeral home.

The Funeral Advantage Program, popularised by Lincoln Heritage Life Insurance Company, is one of the most well-known branded versions of this product. However, the term is now broadly used across the industry to describe any final expense policy tied directly to burial and cremation costs.

Key Characteristics

- Small face amounts: $5,000 to $35,000 sized to cover funeral costs, not replace a salary.

- Whole life structure: Coverage never expires as long as premiums are paid.

- No medical exam: Approval is based on a health questionnaire or is fully guaranteed.

- Level premiums: Your monthly cost is locked in at enrollment and will never increase.

- Fast payout: Most claims are paid within days of death certificate submission.

| Data PointAccording to the National Funeral Directors Association (NFDA), the median cost of a funeral with viewing and burial in 2023 was $8,300. A funeral with cremation averaged $6,971. When you add a cemetery plot ($1,000–$4,000), headstone ($500–$3,000), and reception costs, total expenses routinely exceed $12,000–$15,000 |

How Funeral Advantage Differs from Standard Life Insurance

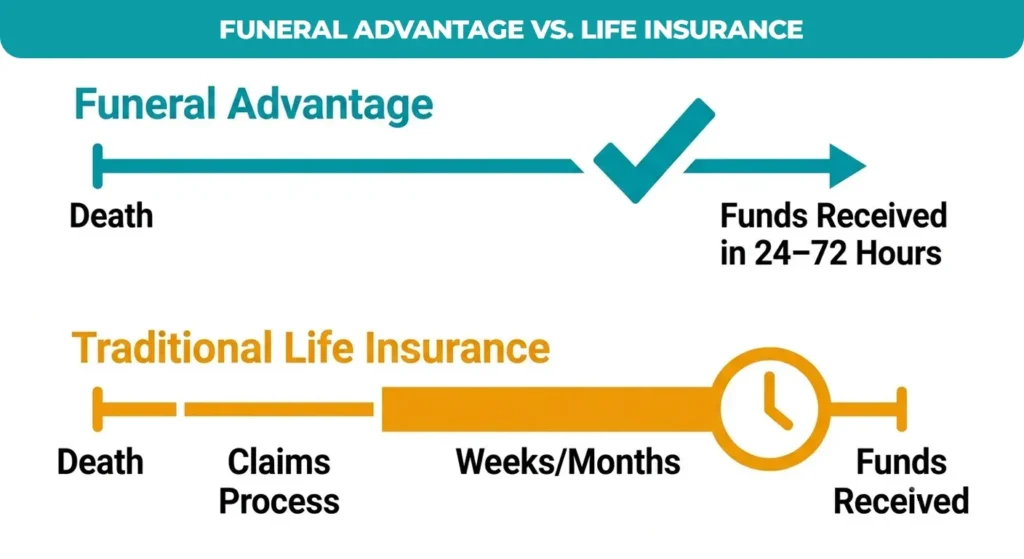

Many people assume their existing term or whole life policy will cover funeral costs. In many cases, it will eventually. But “eventually” is the problem. Standard life insurance claims can take weeks or even months to process, and the payout goes to the named beneficiary as general funds, not directly to a funeral home.

A Funeral Advantage plan is designed for speed and specificity. The table below captures the core differences:

| Feature | Funeral Advantage Plan | Standard Life Insurance |

| Benefit Amount | $5,000 – $35,000 | $100,000 – $1M+ |

| Underwriting | Simplified / Guaranteed Issue | Full medical exam required |

| Primary Purpose | Immediate burial/funeral costs | Long-term income replacement |

| Approval Speed | Days to weeks | Weeks to months |

| Premium Stability | Level – never increases | Varies by policy type |

| Age Eligibility | Typically 50–85 | All ages (health-dependent) |

| Payout Timeline | Fast – often within days | Standard claims process |

Takeaway: If you already hold a large term or whole life policy for income replacement, a Funeral Advantage plan still makes sense as a dedicated, fast-access fund. Think of it as financial triage money available the moment your family needs it, without waiting for a larger policy to process.

Key Benefits of Securing a Funeral Advantage Policy

Ease of Qualification

Most Funeral Advantage plans use simplified or guaranteed-issue underwriting. Simplified-issue policies ask a short health questionnaire, typically 2 to 10 yes/no questions. Guaranteed-issue policies ask nothing at all. This makes them accessible to seniors with chronic conditions like diabetes, COPD, or heart disease who might be declined for traditional coverage.

In our experience, applicants between the ages of 50 and 85 are almost universally able to qualify for some level of coverage. The tradeoff for guaranteed issue is a graded benefit period (explained in a later section).

Speed of Payout

Funeral homes are not charities. They typically require payment or, at a minimum, a signed assignment from an insurance company before services begin. Funeral Advantage policies are built around this reality. Most insurers that specialise in final expense coverage have streamlined claims teams that process payments in 24–72 hours after receiving a valid death certificate and claim form.

Portability

Unlike pre-paid funeral contracts tied to a specific funeral home, a Funeral Advantage insurance policy follows the insured individual. Your beneficiary chooses the funeral home, the services, and the arrangements. If you move to a different state or simply change your preferences, the policy adapts with no renegotiation required.

Understanding Costs and Coverage Amounts

How Much Does the Funeral Advantage Program Cost?

Premium costs vary based on age, gender, health status, and coverage amount. As a general benchmark:

- Age 50, $10,000 coverage: approximately $30–$45/month

- Age 65, $10,000 coverage: approximately $50–$70/month

- Age 75, $10,000 coverage: approximately $90–$130/month

- Guaranteed-issue (any age): 20–30% higher than simplified-issue for equivalent coverage

The most important feature: premiums are guaranteed at a level for life. Unlike health insurance, there are no annual increases. The amount you pay at enrollment is the amount you pay forever.

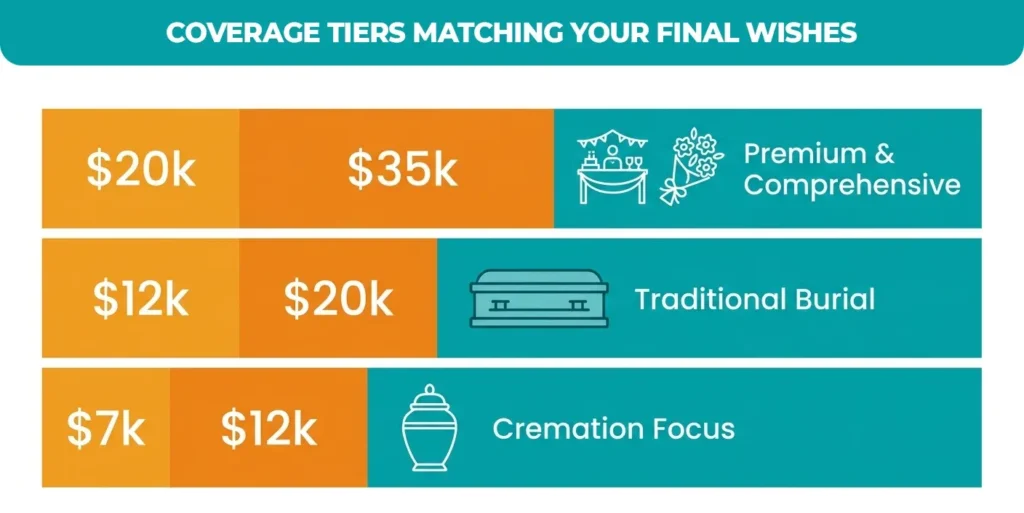

Coverage Ranges and What They Should Cover

Most Funeral Advantage plans offer coverage between $5,000 and $35,000. Your ideal coverage amount depends on your final wishes:

- Cremation-focused plan: $7,000–$12,000 typically covers all costs

- Traditional burial: $12,000–$20,000 recommended minimum

- Premium burial + reception: $20,000–$35,000 for comprehensive coverage

Factors to Consider Before You Buy

Financial Stability of the Insurer

Always verify the financial strength of any insurer before committing. The most reliable rating source is A.M. Best, which grades insurers from A++ (Superior) to D (Poor). For a policy you intend to hold for decades, look for a minimum rating of A- or better. Lincoln Heritage Life, one of the primary Funeral Advantage providers, holds an A- rating from A.M. Best as of 2024.

Graded Death Benefits and Waiting Periods

Guaranteed-issue policies commonly include a graded benefit clause. This means if the insured dies within the first 24 months of the policy (from non-accidental causes), the benefit paid may be limited to a return of premiums plus interest, not the full face amount.

Simplified-issue policies often waive this restriction for applicants who pass the health questionnaire. If you are in reasonably good health, always pursue simplified issues first to avoid the waiting period.

Funeral Advantage: Pros and Cons

| PROS | CONS |

| No medical exam required | Lower coverage ceiling ($35K max) |

| Level premiums for life | Graded benefits in the first 24 months |

| Fast beneficiary payout | Not designed for income replacement |

| Portable – works at any funeral home | Premiums can be higher per dollar vs term |

| Covers cremation or traditional burial | Some policies have age caps at 85 |

| Protects family from emotional overspending | Policy details vary widely by insurer |

Conclusion

Finalising your end-of-life arrangements with a Funeral Advantage plan is a definitive act of love that secures your family’s financial autonomy during their most vulnerable moments. By bypassing the agonising delays of traditional life insurance, these specialised policies provide immediate liquidity to cover essential expenses, effectively shielding your loved ones from the crushing burden of unexpected debt or the stress of emotional overspending.

Taking decisive action today transforms a potential financial crisis into a seamless, dignified transition that preserves your legacy. We strongly encourage you to evaluate your coverage needs against your final wishes and consult with a trusted advisor to lock in level premiums, guaranteeing.

Ready to Secure Your Legacy?

Don’t leave your final arrangements to chance or burden your loved ones with unexpected costs. At Premier Services Agency, we help you navigate the complexities of final expense insurance to find the plan that best fits your budget and wishes. Click Here to Get Your Free Quote.

Frequently Asked Questions

Is the Funeral Advantage Program legit?

Yes, it is a legitimate, licensed insurance product. The program offered through Lincoln Heritage Life Insurance Company, operational since 1956, maintains a strong A- financial rating from A.M. Best.

How much does the Funeral Advantage Program cost?

Monthly premiums depend on your age, gender, health, and coverage amount. For $10,000 in coverage, healthy 65-year-olds typically pay $50–$70, while 75-year-olds may pay between $90 and $130 per month.

What happens to a body if no one can pay for a funeral?

Without family funds, the state may arrange an indigent burial or cremation at public expense. The remains are often interred in a municipal cemetery within a minimally marked, numbered plot.

How much is a $10,000 burial policy?

A $10,000 policy costs roughly $30–$45 monthly for a healthy 50-year-old, increasing for older applicants. Guaranteed-issue policies generally cost 20–30% more than simplified-issue plans, with premiums remaining fixed for life.

Is the government giving $25,000 to seniors for burial?

No, this is a common misconception. The Social Security Administration only provides a one-time $255 death benefit to eligible survivors, making private insurance the most reliable source for end-of-life funding.