Most people plan for retirement by saving diligently, investing wisely, and paying off debt. Far fewer plan for the moment they might need help bathing, dressing, or remembering to take their medication. That gap in planning is where long-term care insurance comes in, and it is a gap that catches millions of families off guard every year, because standard health insurance and Medicare were never designed to cover it.

In short, long-term care insurance is a policy that pays for the non-medical, personal care many older adults eventually need, whether that’s a home health aide, an assisted living facility, or a nursing home, costs that Medicare and most health plans specifically exclude. It exists to protect the retirement savings you’ve spent decades building from being wiped out by a single health event.

This guide breaks down how long-term care insurance actually works, the difference between traditional and hybrid policies, what drives the cost of long-term care insurance, and how to figure out whether it belongs in your own financial plan.

What Is Long-Term Care Insurance and How Does It Work?

Long-term care insurance is coverage for the assistance people need with everyday activities when they can no longer manage independently, not medical treatment in the traditional sense, but hands-on personal care. That distinction matters because it’s precisely the coverage gap that Medicare leaves open (for more on what Medicare does and does not pay for, see our companion guide on Medicare coverage).

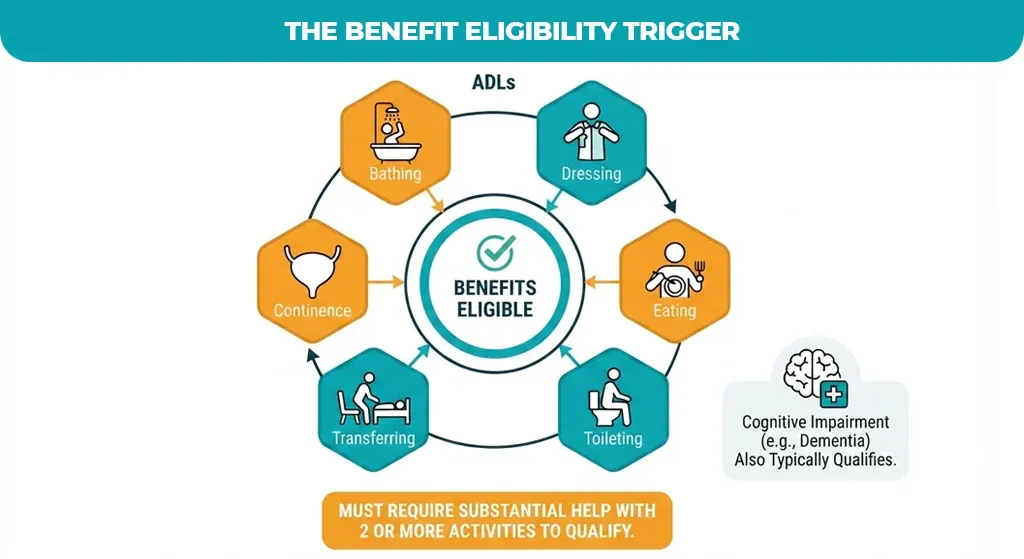

The Six Activities of Daily Living (ADLs)

Insurers determine eligibility for benefits using a standardized list of six Activities of Daily Living. Most policies require that you need substantial help with at least two of the following before benefits begin:

- Bathing

- Dressing

- Eating

- Toileting

- Transferring (moving in and out of a bed or chair)

- Continence

A severe cognitive impairment, such as Alzheimer’s disease or another form of dementia, also typically qualifies a policyholder for benefits, even if they can physically perform all six ADLs. Insurers use industry-standard definitions of “chronic illness” (generally drawn from IRS and NAIC guidelines) to make this determination consistent across policies.

The Elimination Period

Think of the elimination period as the deductible of long-term care insurance, except instead of a dollar amount, it’s measured in days. It is the period of time (usually 30, 60, or 90 days) in which you cover your own medical expenses prior to the insurance company beginning to pay benefits. A longer elimination period generally means a lower premium, but it also means more out-of-pocket exposure early on, so it’s worth weighing against your available savings.

Understanding Your Coverage Options

Not all long-term care insurance policies are structured the same way. The two dominant models, traditional and hybrid, trade off differently on cost, flexibility, and what happens to your money if you never need care.

Traditional Long-Term Care Insurance

A traditional, standalone long-term care insurance policy works much like auto or home insurance: you pay a premium, and if you use the benefit, the policy pays out for covered care. If you never need long-term care, however, those premiums are simply gone; there’s no refund, no death benefit, no residual value. This “use-it-or-lose-it” structure is the single biggest drawback of long-term care insurance that traditional buyers cite.

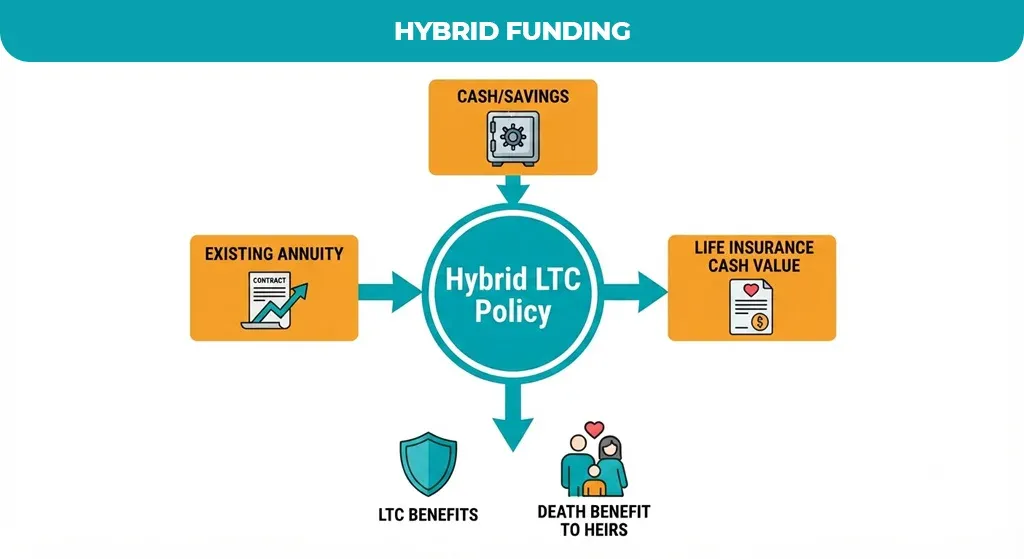

Hybrid (Linked-Benefit) Policies

Hybrid policies link long-term care benefits to a life insurance policy or an annuity, typically funded with a single lump-sum premium or a limited number of payments. If you eventually need long-term care, you draw down the benefit to pay for it. If you don’t, your beneficiaries receive a death benefit instead, so the premium is never simply forfeited. This structure has made hybrid long-term care insurance quotes increasingly popular among buyers.

Traditional vs. Hybrid: A Side-by-Side Comparison

Choosing between traditional and hybrid long-term health care insurance often comes down to how you weigh upfront cost against the certainty of getting something back.

| Feature | Traditional LTCI | Hybrid (Linked-Benefit) |

| Premium structure | Fixed or variable annual premiums | Often, a single lump sum or limited-pay schedule |

| If care is never needed | Premiums are not returned | Heirs receive a death benefit |

| Initial cost | Lower ongoing monthly premiums | Higher upfront cost, but predictable |

| Premium stability | Can rise over time (insurer-approved increases) | Generally fixed once funded |

| Underwriting | Often less strict, more plan variety | Can require significant upfront capital |

Who Should Consider Purchasing Long-Term Care Insurance?

There’s no universal answer to “Is long-term care insurance worth it?” It depends heavily on your assets, health, and family circumstances.

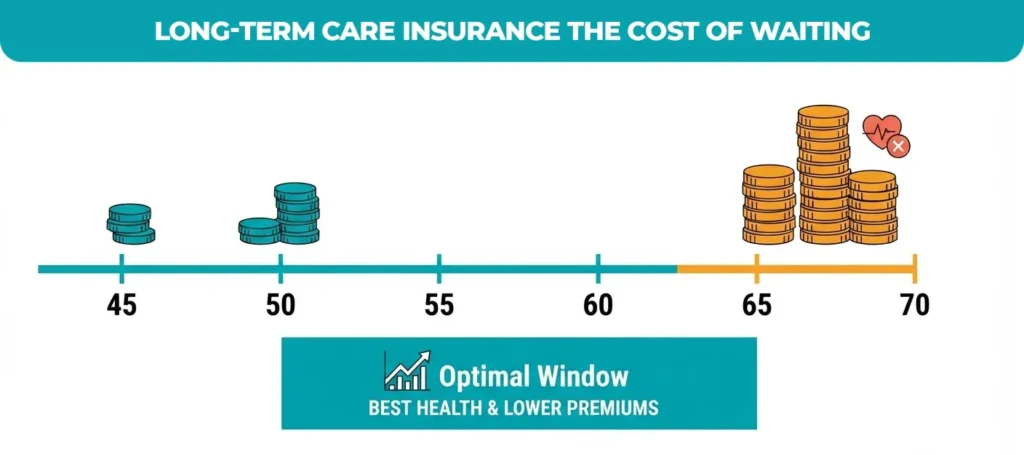

The Sweet Spot: Age 50-65

Most financial professionals point to the window between 50 and 65 as the optimal time to buy. Health is more likely to still qualify for favorable underwriting, and premiums are meaningfully lower than they will be a decade later. Waiting until a health scare prompts the decision often backfires, as a new chronic diagnosis can make a policy unaffordable or unavailable altogether.

Assessing Your Financial Profile

Long-term care insurance tends to make the most sense for people with moderate-to-significant assets enough that a multi-year nursing home stay would meaningfully damage their retirement savings, but not so much that self-funding care out of pocket is a non-issue. On the other end of the spectrum, individuals with very limited assets may eventually qualify for Medicaid to cover long-term care costs, which changes the insurance calculus considerably.

Key Factors That Impact Costs and Benefits

A handful of policy design choices do the most work in shaping both your premium and how well the policy will actually perform when you need it.

Daily or Monthly Benefit Amount

This is the cap on what the policy will pay toward your care costs over a given period. Setting it too low leaves a gap you’ll have to cover yourself; setting it far above local care costs wastes premium dollars.

Benefit Duration

Many advisors recommend a three-to-five-year benefit period rather than unlimited coverage. These days, unlimited policies are uncommon and costly, and ordinary long-term care claims—including those for memory care—usually settle within that three to five-year period, making it a fair compromise between protection and premium cost.

Inflation Protection

Because care costs rise over time, a policy purchased today without inflation protection may cover only a fraction of actual costs by the time you file a claim two or three decades later. Compound inflation riders cost more upfront but are often essential for younger buyers with a long time horizon before they’re likely to need care.

Tax Considerations

Policies that meet federal standards are considered “tax-qualified,” which can make a portion of premiums tax-deductible as a medical expense, subject to IRS age-based limits, and generally allows benefits to be received tax-free. Because tax treatment depends on your individual situation, it’s worth confirming current thresholds with a tax professional before assuming a specific deduction applies.

How to Evaluate and Choose a Policy

Once you’ve decided insurance for long-term care fits your plan, the carrier and policy details matter as much as the decision to buy.

Financial Stability of the Insurer

Because you may not file a claim for twenty or thirty years, the insurer’s long-term financial strength matters enormously. Check independent ratings from agencies such as A.M. Best or Fitch before committing, and favor carriers with a long track record in the long-term care market specifically.

Policy Flexibility and Coverage Scope

Ask whether the policy allows you to adjust coverage later as your needs or budget change, and confirm exactly which care settings are included. The best long-term care insurance policies for most buyers cover home care, assisted living, and memory-care units, not just nursing home stays, since most people prefer to receive care at home for as long as possible.

Conclusion

Protecting your financial future requires addressing the significant gap in coverage left by Medicare and standard health plans. Whether you opt for a traditional standalone policy or a hybrid plan that offers a return of value, long-term care insurance serves as a vital safeguard against potential wealth-depleting health events.

The ideal strategy depends on your unique age, health, and financial circumstances, making professional guidance essential for personalized planning. If you are within the recommended 50-to-65 age window, start gathering quotes now to lock in favorable rates while you are still in good health.