Introduction

If the unexpected happened tomorrow, would your family’s standard of living remain secure? It is a question most households avoid, yet it is the most important financial question a parent or spouse can answer. Family life insurance plans are the cornerstone of a resilient financial foundation. The right plan replaces lost income, eliminates debt, funds your children’s education, and preserves the life you have built, even when you are no longer there to provide it. This guide walks you through everything you need to know in 2026: how to choose between term and permanent coverage, how to calculate your true coverage gap, which riders add real value, and how to avoid the mistakes that leave families underprotected.

Why Families Need Dedicated Life Insurance Plans

Replacing Lost Income

The most immediate risk any household faces after losing a breadwinner is income loss. Life insurance replaces that income stream so surviving family members can maintain their standard of living, service existing debt, and meet future obligations without liquidating assets or depending on relatives. Financial planners generally recommend coverage equal to 10–12 times gross annual income, though the precise figure depends on your household’s unique obligations.

Beyond the Death Benefit

Modern family life insurance plans do far more than pay a lump sum. The death benefit may be set up as follows:

- Pay off the mortgage so the family keeps the home

- Fund a 529 or education savings plan for each child

- Replace the economic value of a stay-at-home parent’s labour (childcare, home management, transportation, often worth $150,000+ per year when priced at market rates)

- Cover outstanding credit cards, personal loans, and student debt

- Provide a bridge income during the surviving spouse’s grief and job-search transition

Comparing Life Insurance Options for Families

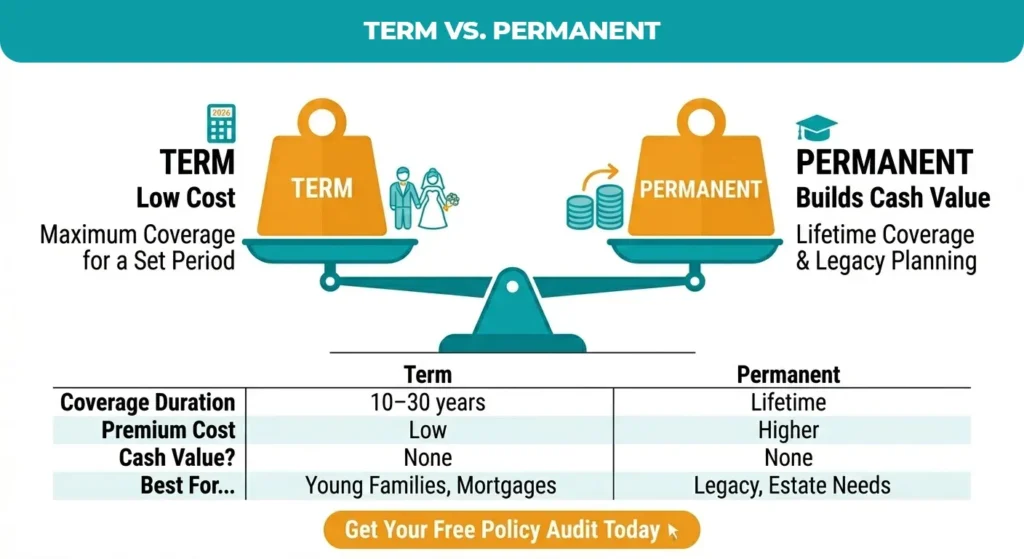

Choosing between term and permanent life insurance is the single most consequential decision in family life insurance planning. Neither is universally superior; the right answer depends on your age, budget, obligations, and long-term financial goals.

Term Life Insurance

Term life insurance provides a death benefit for a defined period, typically 10, 20, or 30 years, at the lowest available premium. It is the most popular choice among young families because it delivers maximum coverage during peak responsibility years at a cost most budgets can absorb. A healthy 35-year-old non-smoker can secure a $500,000 20-year term policy for approximately $25–$35 per month.

Permanent (Whole and Universal) Life Insurance

Permanent life insurance, including whole life and universal life, never expires as long as premiums are paid. It also builds cash value over time, which grows on a tax-deferred basis and can be borrowed against for education costs, retirement supplementation, or emergencies. Premiums are significantly higher than term, but the policy functions as both protection and a long-term financial asset.

Term vs. Permanent: Side-by-Side Comparison

Use the table below to identify which policy structure aligns with your family’s current stage and goals.

| Feature | Term Life | Permanent Life | Best Choice When… |

| Coverage Period | 10–30 years | Lifetime | Depends on the goal |

| Monthly Premium | Low ($20–$50/mo) | Higher ($100–$300/mo) | Budget first |

| Cash Value | None | Yes (grows tax-deferred) | Estate planning |

| Ideal For | Young families, mortgages | Legacy, estate needs | Laddering strategy |

| Convertible | Often yes | N/A | Key flexibility option |

| Death Benefit | Level or decreasing | Level or increasing | Match obligations |

| Best Life Stage | 25–45 years old | 40+ with long view | Review every 5 years |

The Laddering Strategy: A Smart Middle Path

Laddering combines multiple term policies with different expiration dates to match your decreasing financial obligations over time. For example:

- A 30-year, $500,000 policy to cover the mortgage and replace income through retirement age

- A 20-year, $300,000 policy to cover the children’s college years

- A 10-year, $200,000 policy to cover current high-debt years

As each policy expires, your obligations have also decreased, and your total premium cost drops accordingly. Laddering is particularly cost-effective for families who need significant coverage today but expect their financial picture to simplify in 10–15 years. [CITE: LIMRA 2024 Insurance Barometer Study for laddering adoption rates]

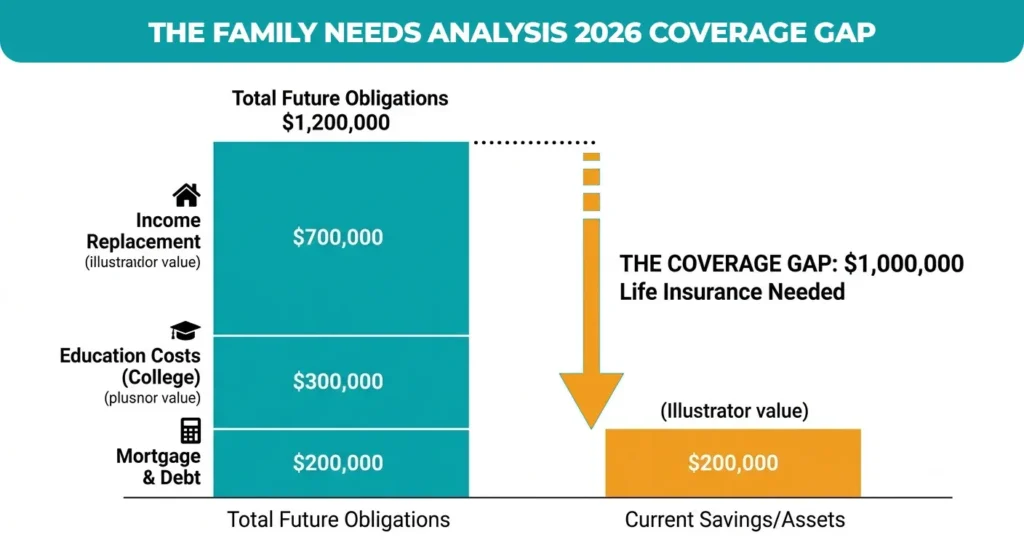

Assessing Your Coverage Needs

No two families have identical insurance needs. A rigorous Family Needs Analysis, not a generic online rule-of-thumb, is the only way to know your actual coverage gap.

Step-by-Step: The Family Needs Analysis

- Calculate total outstanding debt: Add your mortgage balance, car loans, student loans, personal loans, and credit card balances.

- Estimate income replacement: Multiply your annual gross income by the number of years your family will need financial support (typically until the youngest child is financially independent, often 20–25 years).

- Project future education costs: The College Board estimates that four-year private college tuition will average $60,000–$80,000 per year by 2030. Multiply by the number of children and the years until enrollment.

- Account for final expenses: Funeral costs, estate settlement, and medical bills typically run $15,000–$25,000.

| Expert Note: Don’t Forget InflationA coverage amount that feels adequate today may fall short in 15 years. When projecting income replacement and education costs, apply a 3–4% annual inflation rate. [INSERT: Internal link to inflation-adjusted needs calculator] |

Customising Plans with Strategic Riders

Riders are optional add-ons that extend the functionality of a base life insurance policy. For families, the right riders can close critical gaps at a fraction of the cost of a separate policy.

Top Riders for Family Life Insurance Plans

- Child Term Rider: Adds affordable coverage for all children under one rider, typically $10,000–$25,000 per child for a few dollars per month. Upon reaching adulthood (usually age 25), the child can convert to their own permanent policy without a medical exam, a significant advantage for children who may later have health issues.

- Waiver of Premium Rider: If the primary policyholder becomes totally disabled and unable to work, this rider waives all future premiums while keeping the policy fully in force. For families dependent on a single income, this is essential protection.

- Accelerated Death Benefit (ADB) Rider: Allows the policyholder to access a portion of the death benefit if diagnosed with a terminal illness. Provides critical funds for medical care and final arrangements without disrupting other assets.

- Guaranteed Insurability Rider: Allows the policyholder to purchase additional coverage at specified life events (marriage, birth of a child, home purchase) without proving insurability. Critical for younger buyers who expect their needs to grow.

Common Pitfalls When Choosing Family Insurance

Under-Insuring

The most pervasive mistake families make is buying coverage based on what feels affordable rather than what is actually needed. A 2023 LIMRA study found that 41% of American households would face financial hardship within six months of losing the primary earner, a direct consequence of under-insurance. The gap between perceived and actual needs is especially pronounced for dual-income households and families with young children.

Focusing Only on Price

Choosing the cheapest policy without examining its conversion options, carrier financial strength (look for A.M. Best ratings of A or better), or exclusion clauses is a false economy. A low-cost term policy with no conversion rider may leave you uninsurable at term expiration if your health has declined. Always compare policy features alongside premium cost.

Forgetting to Update

Life insurance is not a set-and-forget financial product. Major life events change your coverage needs dramatically. Use the checklist below to identify when a policy review is warranted.

| Life Event Review Your Family Life Insurance Plan | Done? |

| Birth of a child or adoption | ☐ |

| Marriage or divorce | ☐ |

| Home purchase or major refinance | ☐ |

| Significant income change (raise or job loss) | ☐ |

| Starting or selling a business | ☐ |

| Child turning 18 / leaving home | ☐ |

| Ageing parents become dependents | ☐ |

| Policy approaching term expiration | ☐ |

| Significant new debt taken on | ☐ |

| Annual financial plan review | ☐ |

Conclusion

Family life insurance plans are more than just a financial product; they are a fundamental act of love, responsibility, and intentional planning for your family’s future. By securing the right coverage today, you ensure that your loved ones remain protected, financially stable, and empowered to maintain their standard of living regardless of life’s uncertainties.

The journey toward true peace of mind begins with an honest assessment of your family’s specific income, debt, and long-term goals. Do not leave your family’s security to chance—schedule your professional policy audit today to identify any coverage gaps and lock in optimal protection while you are at your healthiest.

Need a Personalised Life Insurance Strategy?

Stop guessing which plan is right for your family. The expert team at Premier Services Agency compares top-rated carriers to find you the best balance of coverage, cost, and long-term security.

Frequently Asked Questions

What is the best life insurance for a family?

Most families benefit from a laddered combination of term policies, providing high coverage during peak years. Adding a permanent policy supports estate planning goals, ensuring protection is always calibrated to your unique needs.

Is it possible for someone with a pacemaker to obtain life insurance?

Yes, in most cases. Underwriters evaluate the underlying condition, stability, and overall health profile rather than the device itself. Working with an independent broker helps you find carriers that offer the best possible rates.

Can you get life insurance if you have cirrhosis?

While challenging, it is not impossible. Approval depends on the type, severity, and stability of the condition. Consulting a licensed broker experienced in high-risk underwriting is essential to navigating your specific coverage options.

What is the monthly cost of a $100,000 life insurance policy?

Healthy individuals often secure $100,000 in term coverage for $8–$15 monthly. Permanent coverage costs significantly more due to cash value components, though most families require much higher total death benefits for complete income replacement.