When you’re planning for your family’s financial future, life insurance is often the cornerstone of that plan. But a question that trips up even experienced policyholders is simple: Is life insurance taxable?

In most cases, no. A death benefit paid as a lump sum to a named beneficiary is not taxable income. But there are real exceptions to interest, cash value gains, transfer-for-value sales, and estate inclusion that can turn part of a payout into a tax bill if you’re not careful. This guide walks through exactly when life insurance is taxable and when it isn’t, so you can plan with confidence.

Are Life Insurance Death Benefits Taxable?

For most families, this is the core question, and the answer is reassuring: a life insurance death benefit taxable event is the exception, not the rule. The IRS generally excludes death benefits from a beneficiary’s gross income, which means you typically don’t report the payout on your tax return at all.

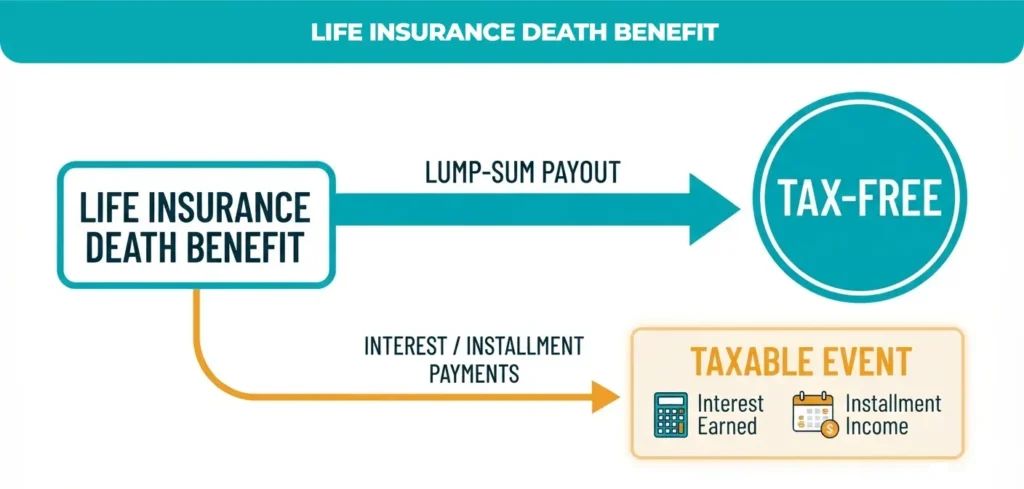

Lump-Sum Payouts

When a beneficiary takes the full death benefit in one payment, it is not considered taxable income under federal law. This is true whether the policy is term, whole, or universal life, and it’s the scenario most people mean when they ask whether the taxable status of life insurance proceeds applies to them. It usually doesn’t.

The Interest Exception

Here’s where people get caught off guard. If the insurance company holds the death benefit for any period before distribution, sometimes at the beneficiary’s request and pays interest on that balance, the interest itself is taxable income, even though the original benefit remains untouched. So if someone asks, is life insurance money taxable in every circumstance, the honest answer is: the principal usually isn’t, but interest earned on it always is.

Installment and Annuity-Style Payments

Beneficiaries who elect to receive the payout over time, rather than as a lump sum, will find that each installment is split into two pieces: a pro-rata portion of the original death benefit (tax-free) and an interest component (taxable). This structure applies whether the choice is made by the policyholder in advance or by the beneficiary after the fact.

When Is a Payout from Life Insurance Taxable?

While a life insurance payout taxable scenario is uncommon for ordinary policies with individual beneficiaries, several specific situations can trigger a tax bill.

The Transfer-for-Value Rule

If you purchase an existing policy from someone else for cash or other valuable consideration, a scenario common in business buy-sell agreements or life settlements, the death benefit can lose its tax-free status. The portion exceeding what you paid for the policy, plus any premiums paid afterward, becomes taxable to you as the new owner. Certain exceptions apply, such as transfers to the insured, a partner of the insured, or a partnership in which the insured is a partner.

Estate Taxes and Ownership Structure

If the deceased person owned the policy at death, or if the beneficiary named is “my estate,” the proceeds can be pulled into the taxable estate. Federal estate tax only applies above a high exemption threshold, which is adjusted periodically, so check current IRS guidelines rather than relying on a number that may be outdated. However, several states apply their own estate or inheritance taxes with meaningfully lower thresholds, so a policy that escapes federal tax can still trigger state-level tax.

Policy Ownership Mismatches

When the person insured is not the person who owns the policy, for example, a parent owns a policy on an adult child, or a business owns a policy on an employee, the transfer of ownership or the eventual payout can create unexpected gift or income tax consequences. This is an edge case that many policyholders overlook until it’s too late to restructure.

Cash Value Life Insurance: Taxable or Not?

Permanent policies, such as whole life, universal life, and variable universal life, build cash value alongside the death benefit. Depending on how you obtain that value, cash value life insurance may or may not be taxable.

Tax-Deferred Growth

Cash value grows without current taxation as long as it stays inside the policy. This tax-deferred compounding is one of the main reasons people ask about whether whole life insurance is taxable in the first place. The growth itself isn’t a taxable event.

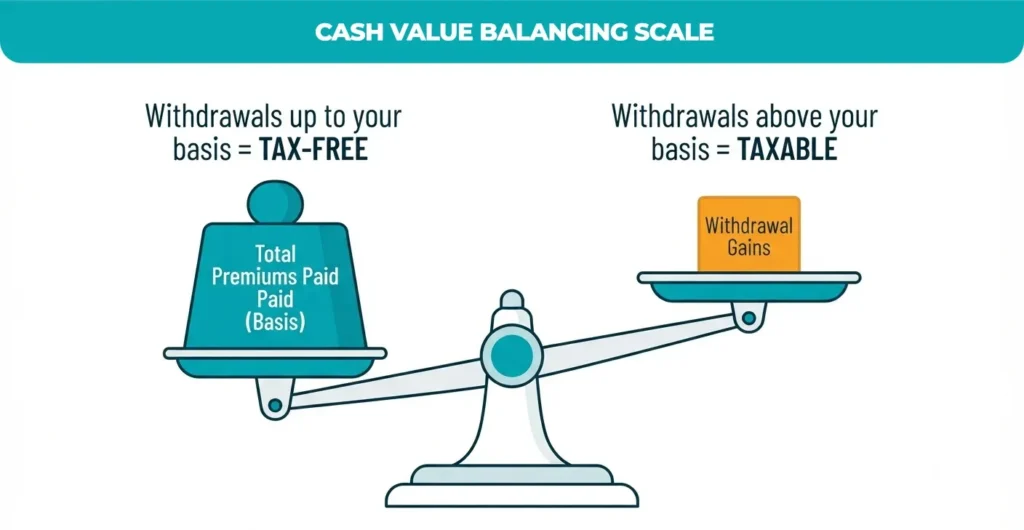

Withdrawals: Basis First, Then Gains

You can generally withdraw an amount equal to your basis for the total premiums you’ve paid without owing tax. Anything withdrawn beyond that basis is taxed as ordinary income. This is the same principle that answers whether the cash value of life insurance is taxable when you take a partial withdrawal instead of a loan.

Policy Loans

Borrowing against your cash value is typically tax-free while the policy remains in force, because a loan isn’t income. The important caveat: if the policy lapses or is surrendered while a loan is outstanding, any loan balance exceeding your basis is treated as taxable income, sometimes producing an unpleasant surprise for policyholders who let an older policy lapse without realizing a loan was attached.

Surrendering the Policy

If you cancel a policy entirely, the question of whether the cash surrender value of life insurance is taxable comes down to simple math: subtract your total premiums paid from the surrender value you receive. If the result is positive, that gain is taxed as ordinary income. If you’ve paid in more than you receive back, there’s no taxable event.

Is Group Term Life Insurance Taxable?

Many employees receive life insurance as a workplace benefit and assume it follows the same rules as an individually purchased policy. It mostly does, with one notable wrinkle: whether group term life insurance is taxable depends on the amount of coverage. The IRS allows the first $50,000 of employer-provided group term coverage to be received tax-free.

Taxable Scenarios at a Glance

| Scenario | Usually Taxable? | Why |

| Lump-sum death benefit paid to a named individual | No | According to IRC Section 101(a), excluded from gross income |

| Interest earned while the benefit is held by the insurer | Yes | Interest is separate from the tax-free principal |

| Policy sold for cash (transfer-for-value) | Often, partially | Gain above the basis plus purchase price becomes taxable |

| Estate named as the beneficiary | Possibly | Proceeds may be pulled into the taxable estate |

| Cash value withdrawal above the basis | Yes | Gain above premiums paid is ordinary income |

| Policy loan (policy stays in force) | No | Loans aren’t income as long as the policy is active |

Strategies to Minimize Tax Liability

Use an Irrevocable Life Insurance Trust (ILIT)

Placing a policy inside an ILIT removes it from your personal estate, which can eliminate federal and state estate tax exposure on the payout. Because the trust, not you, owns the policy, the proceeds generally bypass your taxable estate entirely.

Name Individuals, Not Your Estate

Naming specific people as beneficiaries rather than “my estate” keeps the payout out of probate and reduces the odds that the proceeds get swept into an estate tax calculation.

Coordinate Ownership Carefully

If a policy involves a business, a trust, or a family member other than the insured, review the ownership structure before a claim is ever filed. Mismatched ownership is one of the more overlooked reasons a death benefit taxable event happens at all.

Work With a Tax Professional

Tax law changes, and thresholds for estate and gift tax exemptions are adjusted over time. A CPA or financial advisor who reviews your actual policy documents can confirm whether your specific situation lines up with current IRS rules. General articles like this one are a starting point, not a substitute for personalized advice.

Conclusion

For the vast majority of families, a life insurance payout arrives exactly as intended: tax-free and available when needed most. While most death benefits are exempt, understanding when life insurance is taxable is essential to avoid surprises related to interest, cash value gains, transfer-for-value sales, or estate inclusion.

By proactively managing your ownership structure and beneficiary designations, these potential tax events are largely avoidable. Ultimately, staying informed on whether life insurance is taxable in your specific situation ensures your policy continues to protect your family’s financial future without triggering unexpected tax liabilities.